What Is Cash Damming in Canada? A Complete Guide for Homeowners and Investors

What Is Cash Damming in Canada? A Complete Guide for Homeowners and Investors

Most Canadian homeowners focus on paying down debt faster.

Sophisticated real estate investors often focus on something different: making their debt tax-deductible.

That is where cash damming enters the picture.

The cash damming strategy has become increasingly popular among Canadian investors who own rental properties and want to improve tax efficiency without selling assets or drastically changing their lifestyle.

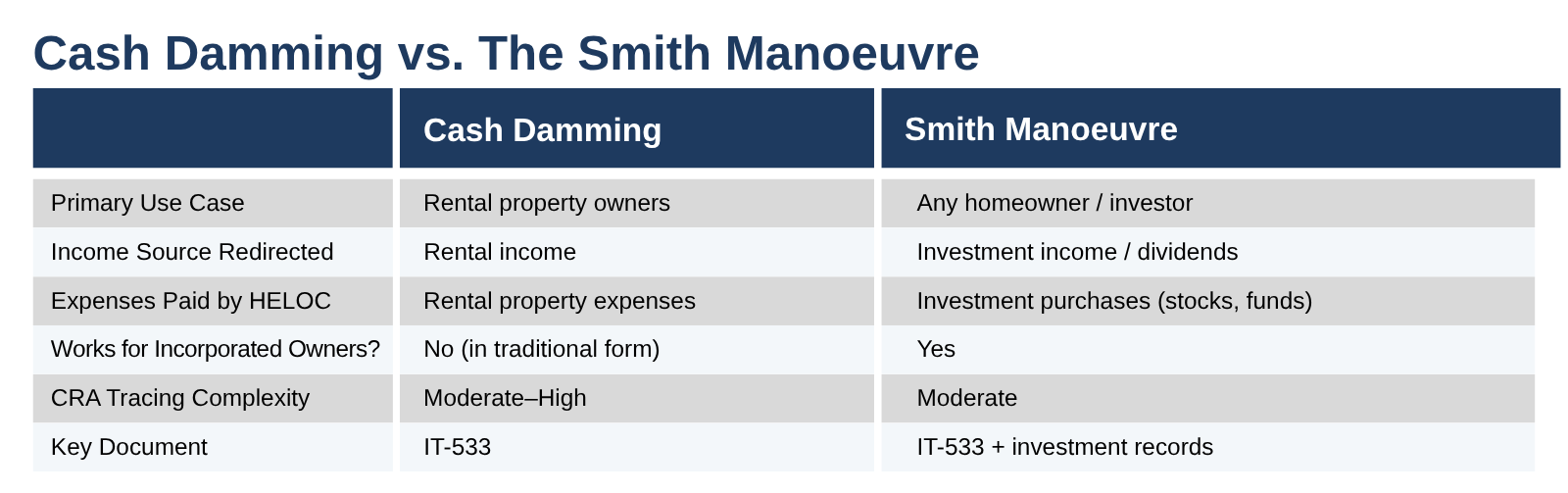

Done properly, cash damming can help convert non-deductible personal debt into deductible investment debt over time. It is commonly used alongside a HELOC and is often compared to the Smith Manoeuvre.

But despite the growing interest, many Canadians still misunderstand how it works, who it is for, and where CRA scrutiny can become a problem.

This guide breaks down the mechanics, tax implications, risks, bookkeeping requirements, and real-world numbers behind cash damming in Canada.

What Is Cash Damming?

Cash damming is a Canadian tax strategy that restructures how rental property expenses are paid.

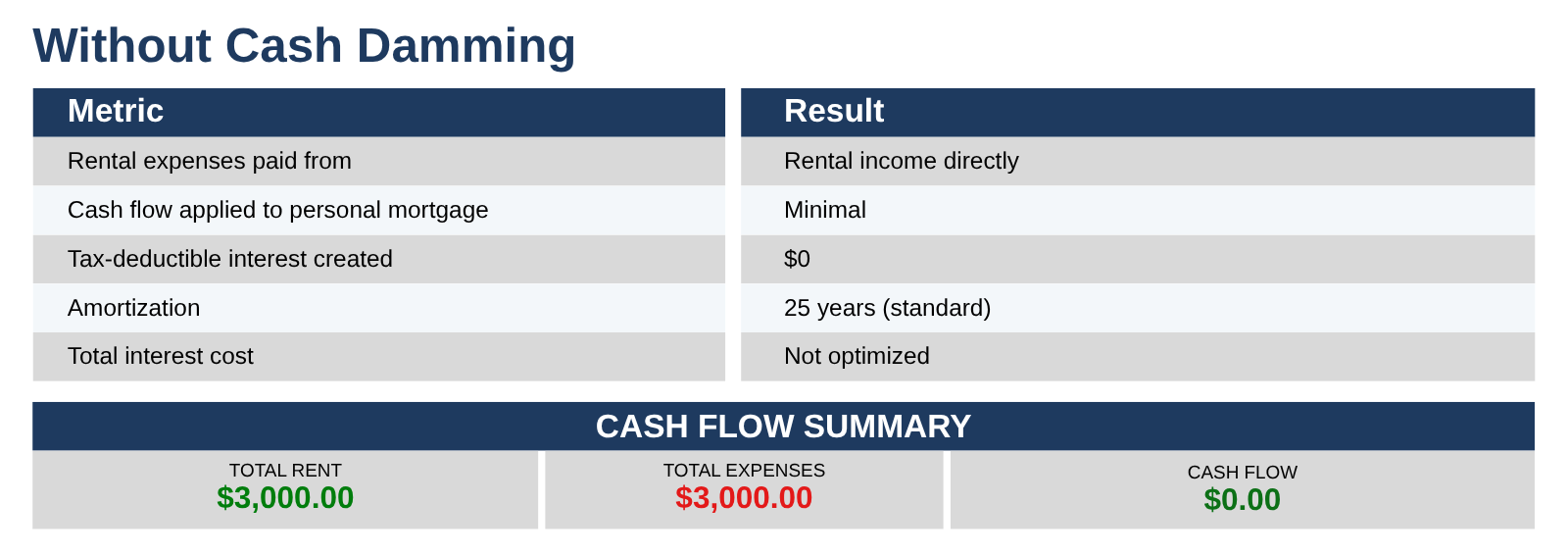

Instead of using rental income to cover rental expenses directly, investors borrow money through a HELOC or re-advanceable mortgage to pay eligible rental expenses. The rental income that would normally cover those expenses is then redirected toward paying down personal, non-deductible debt such as:

A primary residence mortgage

Personal loans

Car loans

Lines of credit

Credit card debt

Over time, more debt shifts from non-deductible to tax-deductible.

The key advantage is that interest on money borrowed for investment purposes may be tax-deductible under Canadian tax law, as acknowledged by the CRA in Interpretation Bulletin IT-533.

How Cash Damming Works: Step by Step

Step 1: Open a HELOC or Re-Advanceable Mortgage

Most investors use a home equity line of credit attached to their primary residence, or a re-advanceable mortgage product that automatically increases HELOC room as the mortgage balance decreases.

Major Canadian lenders including RBC, TD, and Scotiabank offer HELOC products tied to home equity.

Step 2: Use Borrowed Funds for Rental Expenses

Instead of paying rental expenses from personal cash flow or rental income, the investor pays them using borrowed funds from the HELOC.

Eligible expenses typically include:

Mortgage interest on the rental property

Property taxes

Insurance

Repairs and maintenance

Condo fees

Utilities

Property management fees

The CRA generally allows interest deductibility when borrowed money is used to earn income from a business or property. This is the foundation the entire strategy is built on.

Step 3: Redirect Rental Income to Personal Debt

Rental income is then redirected entirely toward non-deductible personal debt — typically the primary residence mortgage.

This gradually converts non-deductible debt into deductible debt over time.

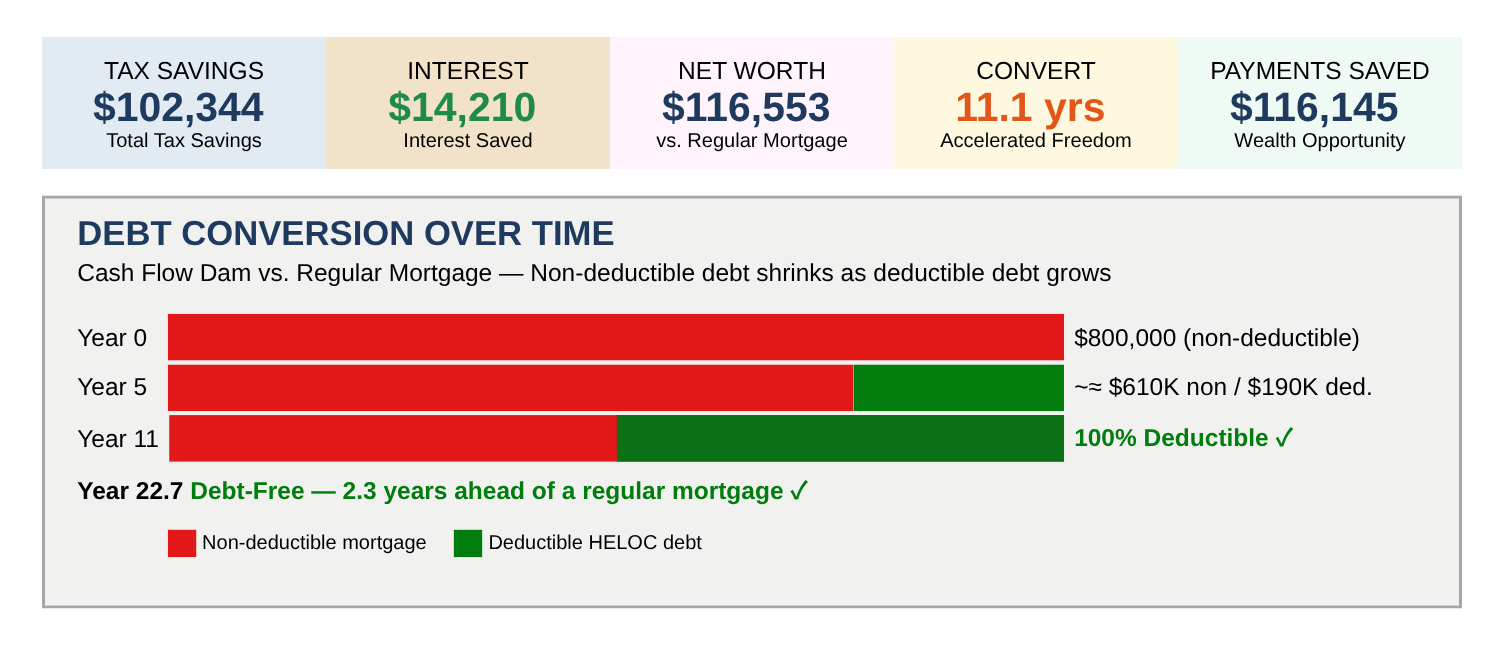

Real Numbers: Cash Damming Example at 40% Marginal Tax Rate

Here is a realistic example based on a Canadian rental property owner. These numbers reflect an actual scenario modeled through a cash damming calculator.

What These Numbers Mean

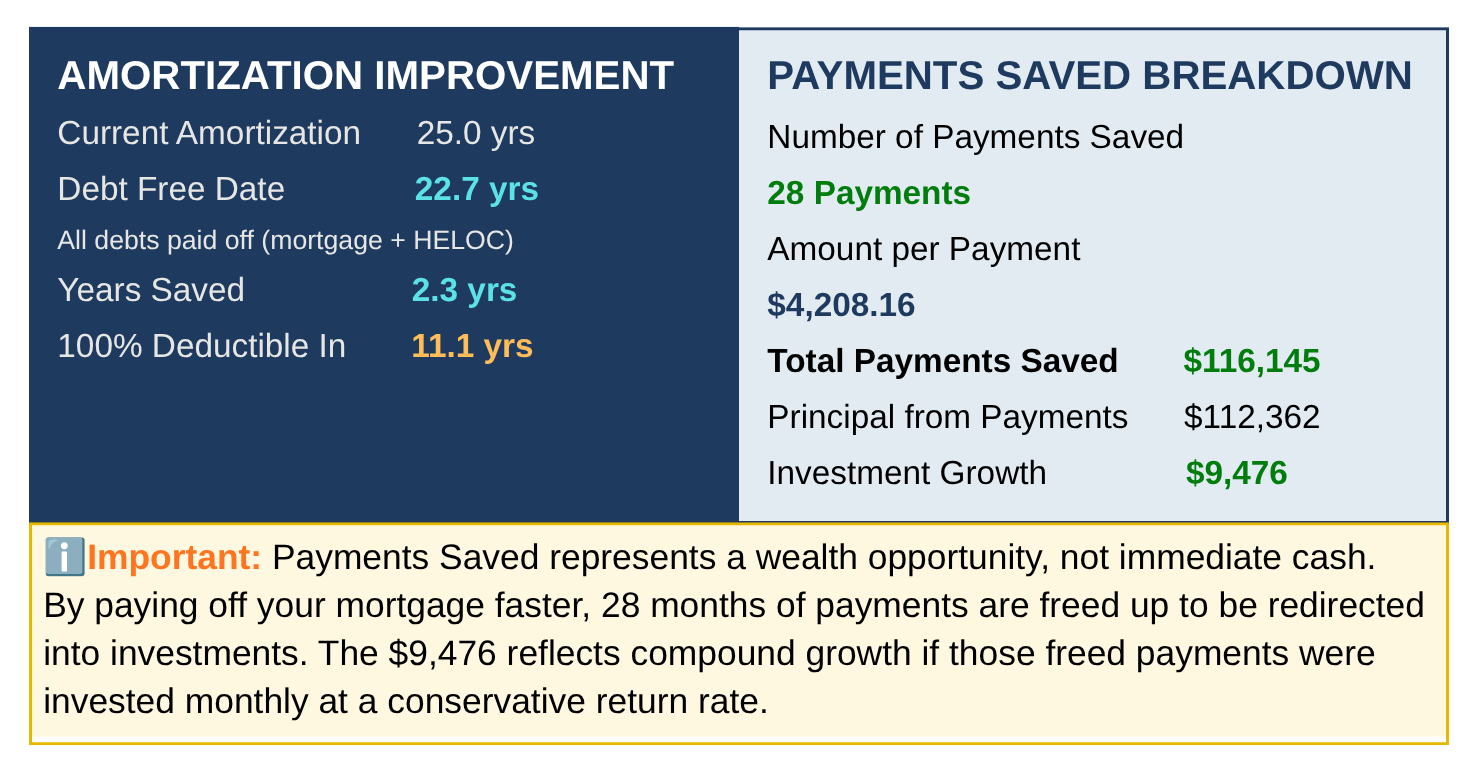

Even at breakeven cash flow ($0/month net from the rental), cash damming still generates $102,344 in tax savings and converts 100% of the debt to deductible within 11 years.

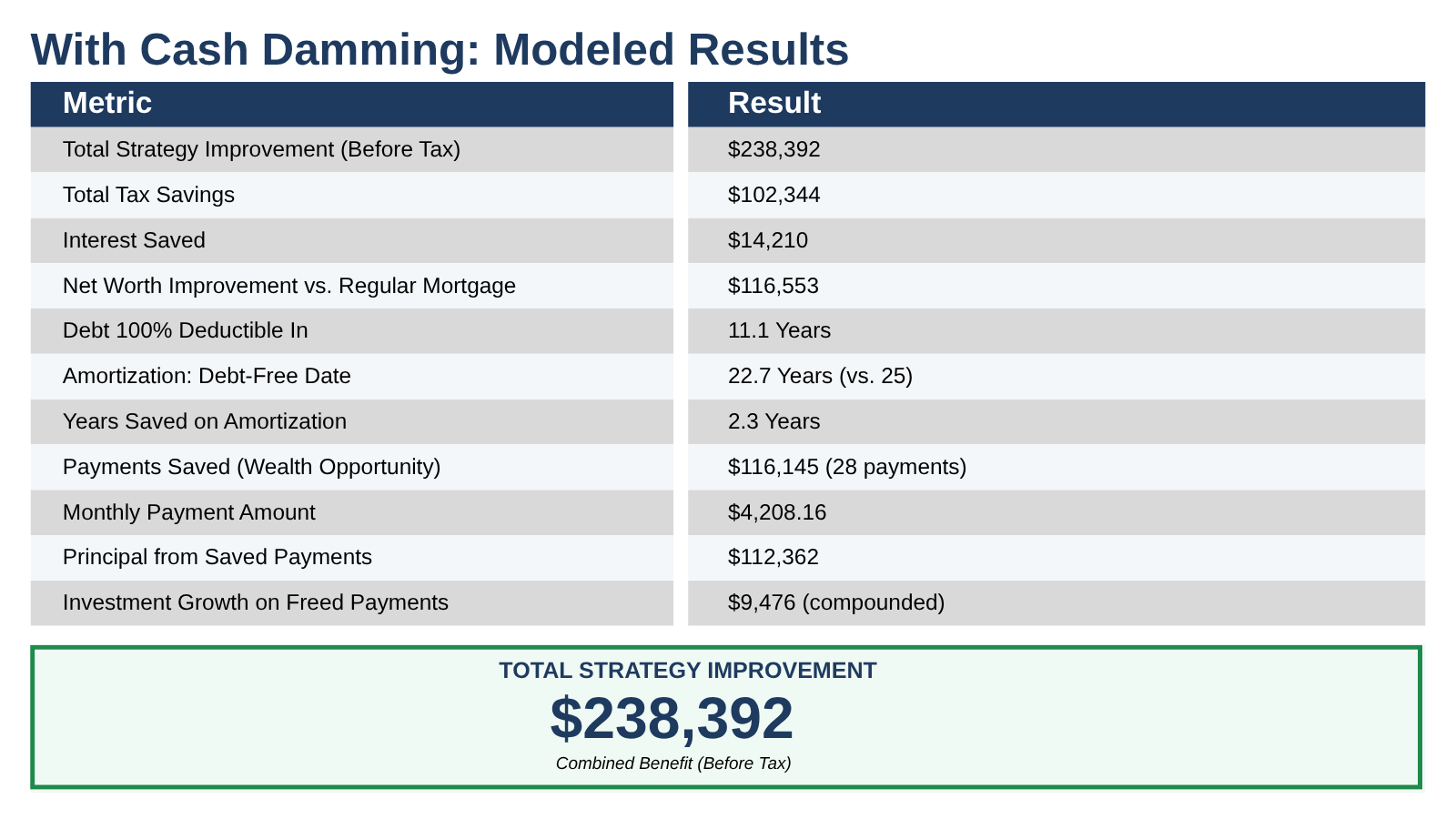

The strategy does not require positive cash flow to work. It requires discipline, proper structure, and clean documentation.

The $116,145 in 'payments saved' is a wealth opportunity — not cash in your pocket today, but freed-up mortgage payments that can be redirected into investments at the end of the strategy, compounding further over time.

CRA Compliance: What You Must Get Right

The strategy only works if the interest tracing is clean. This is where most people make costly mistakes.

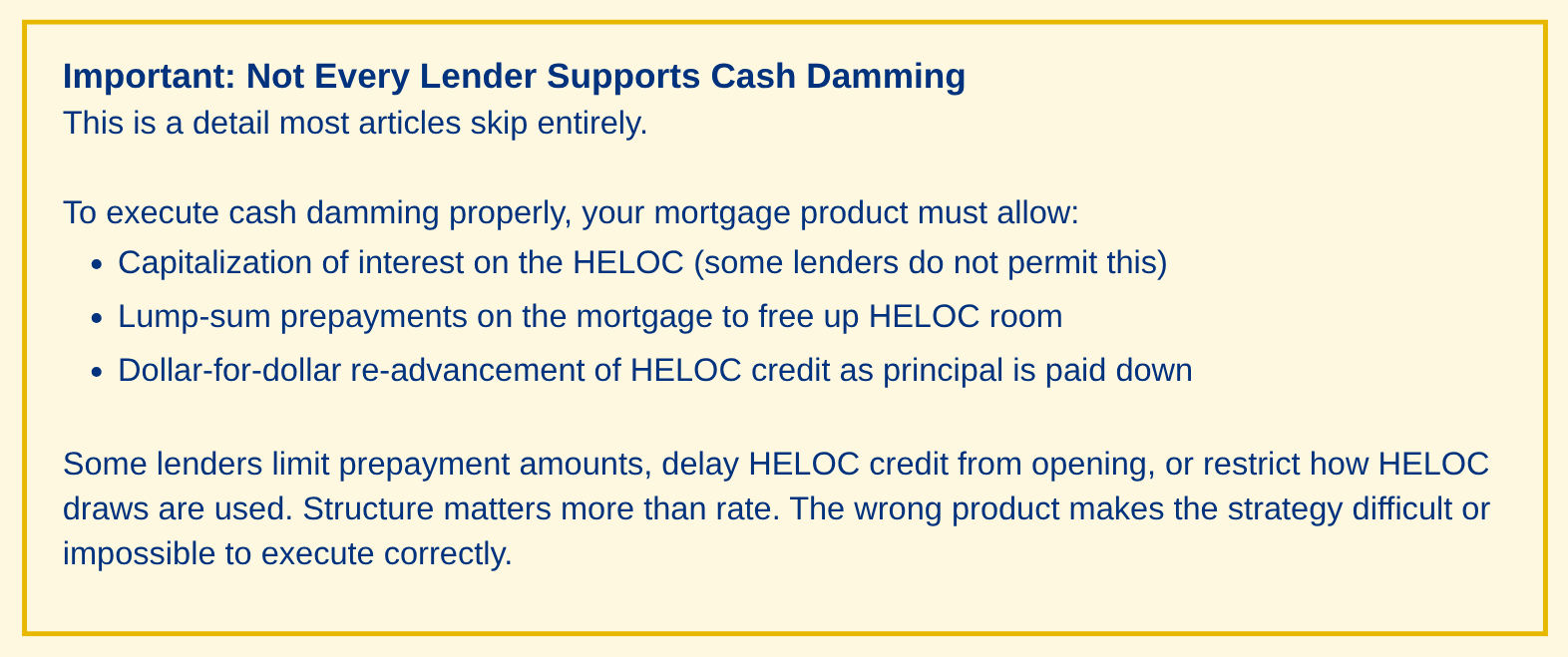

The CRA requires you to prove that borrowed HELOC funds were used exclusively for income-generating purposes. If you cannot demonstrate a clear, unbroken trail from the borrowed dollars to eligible investment expenses, your deductions can be denied.

Required Documentation

Keep rental income and HELOC draw accounts completely separate

Document every HELOC withdrawal with a clear purpose note tied to a specific rental expense

Match HELOC advances to invoices and receipts

Never use the HELOC for personal spending — even a single personal transaction compromises the entire deductibility trail

Maintain all records for a minimum of six years

Commingling funds is the fastest way to lose your deductions and invite a CRA audit.

⚠️ Do Not Attempt Cash Damming Without Professional Guidance

Cash damming involves complex tracing requirements, mortgage product selection, and ongoing bookkeeping that most homeowners and investors are not equipped to manage alone.

Errors in execution — even small ones like a single personal HELOC transaction — can unwind years of work and expose you to CRA reassessment.

Before implementing this strategy, speak with:

A qualified mortgage professional who understands re-advanceable products and CRA tracing rules

A tax advisor or accountant familiar with the IT-533 Interpretation Bulletin

This is not a DIY strategy.

Is Cash Damming Right for You?

The Strategy Works Best For:

Rental property owners with recurring, eligible expenses

Homeowners carrying significant primary residence mortgage balances ($300K+)

High-income earners in the 40%+ marginal tax bracket

Investors who are disciplined with bookkeeping and account separation

Those with a stable rental income, even if the net cash flow is low or breakeven

The Strategy May Not Be Suitable For:

Investors with inconsistent or highly seasonal rental income

Homeowners planning to sell within 2–3 years

Those uncomfortable maintaining strict financial separation and documentation

Owners carrying minimal mortgage debt where implementation costs outweigh the benefit

Incorporated property owners (different rules apply — see the Smith Manoeuvre instead)

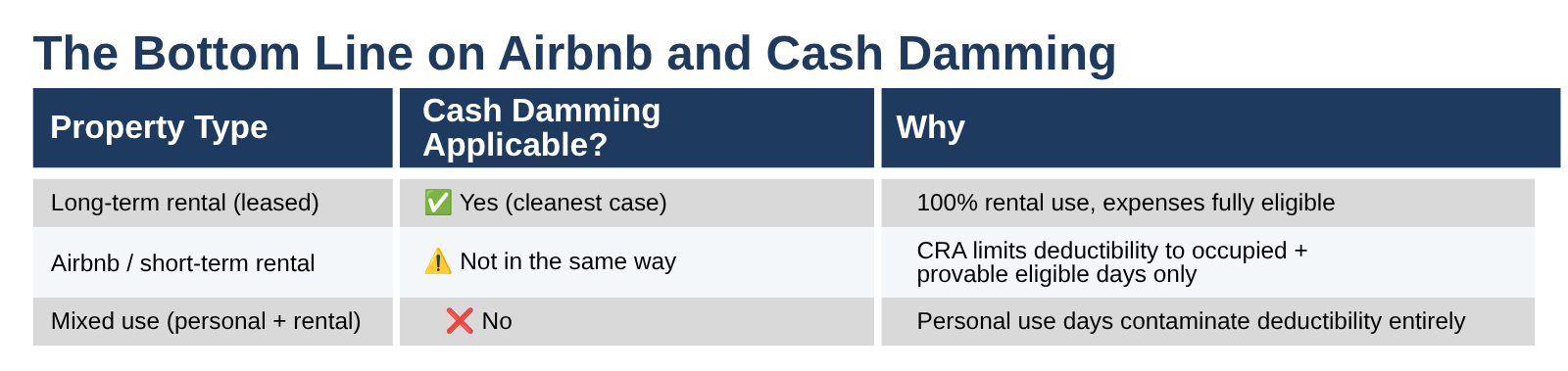

Why Cash Damming Does Not Work the Same Way with Airbnb

This is one of the most common mistakes I see investors make. If your property is listed on Airbnb or any other short-term rental platform, do not assume cash damming applies the same way as a standard long-term rental. It does not.

The Core Problem: CRA's Eligible-Use Test

Cash damming works because borrowed HELOC funds are used to pay expenses for an income-generating property. The CRA allows you to deduct interest on borrowed money used to earn income — but only to the extent that the property is actually being used for that purpose.

For a long-term rental, this is straightforward. The property is rented year-round, expenses are incurred year-round, and the tracing is clean.

For an Airbnb, the CRA looks at actual use, not potential use. And that creates a major problem.

What the CRA Typically Will and Won’t Accept for Short-Term Rentals

Based on anecdotal conversations with Smith Manoeuvre–certified accountants who have navigated CRA audit issues involving Airbnb properties, the CRA will typically accept expenses — and by extension HELOC interest — proportional to:

Days the property was actually occupied by paying guests

Provable days the property was unavailable due to maintenance, cleaning, or necessary repairs directly tied to rental activity

The CRA will typically NOT accept a full 365-day expense claim just because the listing was active or available.

If your Airbnb was occupied 120 days and you can document 15 days of maintenance and turnover, the CRA may only recognize 135 out of 365 days as eligible — roughly 37% of annual expenses.

Borrowing 100% of annual expenses through your HELOC and claiming full deductibility on that interest is the mistake. You can only deduct interest proportional to eligible-use days. The rest is personal.

Important: This is not tax advice. This section is based on anecdotal conversations with Smith Manoeuvre–certified accountants about audit situations they have encountered with short-term rental clients — not a formal CRA position or legal interpretation. Do your own due diligence and speak with a qualified accountant before drawing any conclusions about your specific situation.

Why This Breaks the Cash Damming Structure

Cash damming requires a clean, one-to-one tracing: 100% of borrowed HELOC funds go to 100% deductible rental expenses. If only a portion of your expenses are eligible, you cannot borrow the full expense amount through the HELOC and claim full deductibility. The math falls apart, and more importantly, the CRA tracing falls apart.

You would need to calculate your eligible-use percentage each year, borrow only that portion through the HELOC, and fund the rest personally. At that point, the administrative burden is high, the deduction is partial, and the risk of commingling — already the most dangerous pitfall in cash damming — increases significantly.

If you run short-term rentals and want to improve tax efficiency, there are strategies available — but cash damming is not the right tool. Book a call to discuss what actually fits your structure.

Next Steps

If you think cash damming may be relevant to your situation, here is where to start:

Gather your current mortgage details, rental income, and expense records

Book a consultation to assess whether your current mortgage product supports the strategy

Work with a qualified mortgage professional and tax advisor simultaneously — both sides need to be in sync

Set up proper account separation and tracking systems from day one before the first HELOC draw

Ready to Find Out if Cash Damming Works for Your Situation?

I’ll review your mortgage structure, equity position, and whether cash damming is the right fit for your situation. Book a free assessment below!

⚠️ Legal / Tax / Financial Disclaimer

This article is for educational purposes only.

Nothing in this article constitutes financial advice, mortgage advice, tax advice, or legal advice. Cash damming is a highly technical strategy that requires a properly structured re-advanceable mortgage, strict CRA tracing compliance, and professional coordination between your mortgage agent and accountant.

Do not attempt to implement this on your own. Tax laws and CRA interpretations can change. Always consult qualified professionals who can assess your specific structure and situation before taking any action.

Austin Yeh is a Smith Manoeuvre Certified Professional and independent mortgage agent based in Toronto, funding mortgages across Canada. He specializes in advanced mortgage strategies for high-income earners, real estate investors, and self-employed borrowers.

Lender features and policies are subject to change. Always verify current product details directly with the lender or through an SMCP-certified mortgage broker. This article is for educational purposes and does not constitute financial or mortgage advice.