Everyone's too negative on real estate

Everyone wants a simple answer: is the market recovering or not?

The honest answer - it's not recovering. But it might be closer to a bottom than almost anyone is willing to admit right now. And the gap between what the data is showing and what the headlines are saying is worth paying attention to.

Let me break it down.

Who Is NOT Driving Demand Right Now

#1 Investors are largely out.

Rents are declining. Cap rates are compressed. Sentiment is the worst it's been in years.

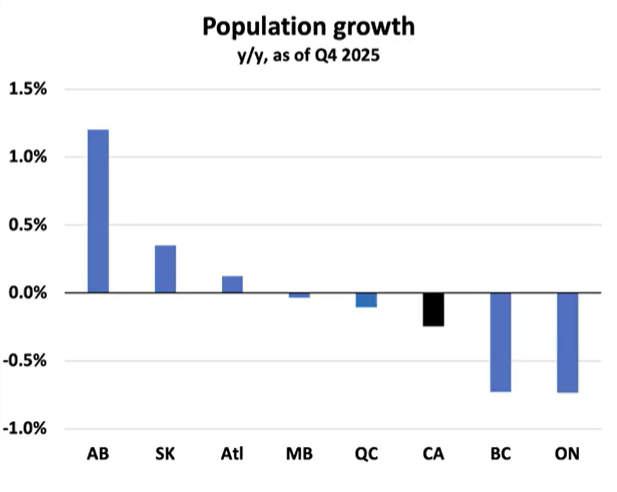

Here's the structural problem: the majority of housing under construction right now is purpose-built rental. At the same time, the non-permanent residents who drove rental demand over the past three years are leaving the country. Ontario and BC are both showing negative population growth year-over-year as of Q4 2025.

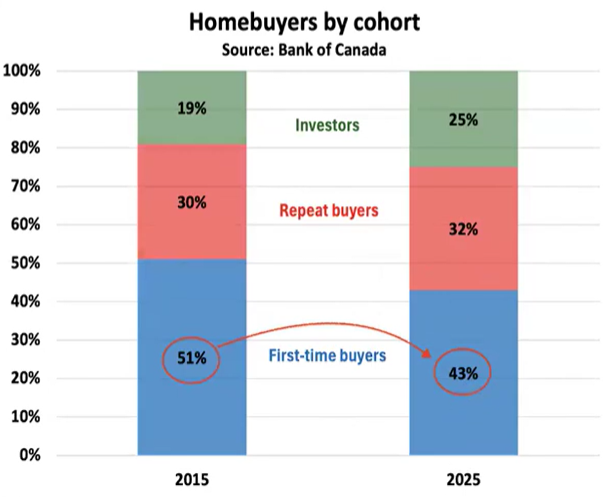

You have increasing supply hitting a market with deteriorating demand. Investors who made up 25% of buyers in 2025 — up from 19% in 2015 — have correctly figured this out and moved to the sidelines.

#2 Repeat buyers are stuck.

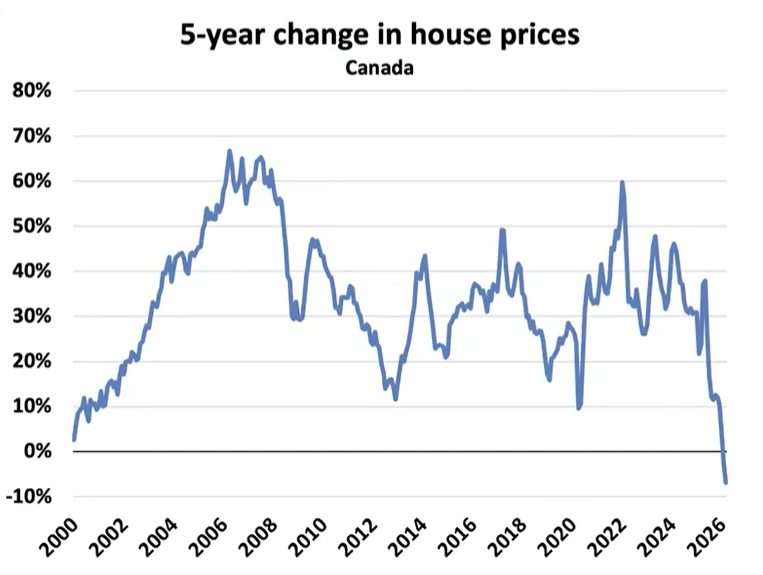

Most homeowners move every 5–7 years. But if you bought anywhere between 2020 and 2022 in Ontario, you're likely sitting at break-even or a loss. Canadian house prices just went negative on a 5-year rolling basis for the first time on record.

And even if someone wanted to move, the math doesn't work. The friction cost of moving laterally in Toronto is brutal. Think about what it actually costs on a $1.2M home:

Realtor fees (both sides): ~$60,000

Double land transfer tax (city + provincial): ~$38,000

Mortgage penalty mid-term: $10,000–$25,000

Legal and misc: ~$5,000

You're writing a $110,000–$130,000 cheque just to end up in a similar house. Most people won't do it unless they have a compelling reason. Right now, most don't.

First, Who Is GOING to be Driving Demand

#1 First-time buyers — and they're already starting to show up.

Their share of transactions dropped from 51% in 2015 to 43% in 2025. Not because they gave up on homeownership — because they got priced out and waited. Every major survey still shows Canadians want to own. They haven't changed their minds. They've delayed.

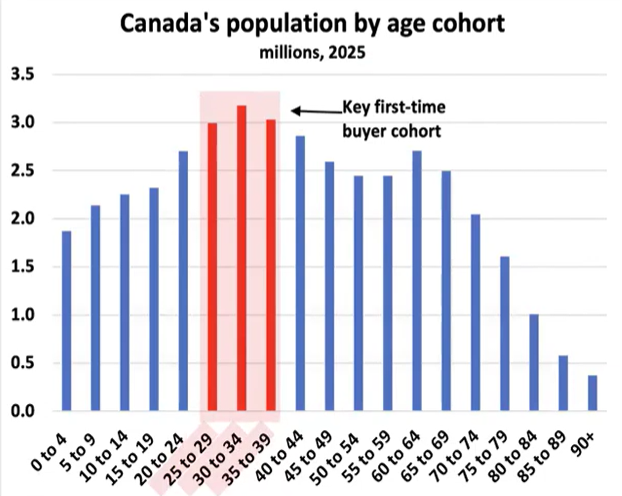

Here's the demographic reality most people are sleeping on: the average age of a first-time buyer in Canada is now 36, and closer to 40 in Ontario.

The 30–39 cohort is the single largest population group in the country right now — roughly 3 to 3.2 million people per five-year band. These are not people who've decided renting is a lifestyle. They're people who got priced out in 2021–2022, watched prices correct 20–25% from peak, and are now quietly asking: is now the time?

The data is suggesting some of them are already pulling the trigger. GTA home sales were up 6.1% month-over-month in April — the largest single-month jump since mid-2025 — and up 7% year-over-year. The real surprise: 416 condo sales were up 14% year-over-year, at the same time that active condo inventory fell 16%. The best explanation for that combination is first-time buyers off the sidelines. Prices are lower. Rates are lower than the peak. The window feels real.

#2 Estate sales and downsizers — the most underappreciated story in Toronto real estate.

Nearly a quarter of detached homes in Ontario are owned by people 75 and older. That cohort is moving — to assisted living, to smaller units, or passing wealth to the next generation. You can see it in the TRREB data: listings flagged as "executor" or "estate" have gone from roughly 5,000 per year in 2016 to over 11,500 in the past 12 months.

These aren't just listings — they create transactions. The adult children inheriting or receiving gifted equity often become the next wave of buyers.

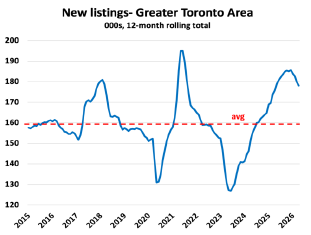

THE SUPPLY SIDE IS QUIETLY TIGHTENING

GTA new listings ran well above the long-run average of roughly 160,000 annually through most of 2025. That trend is rolling over. New listings were down 9.3% year-over-year in April.

Single-family completions across Ontario have collapsed. The "supply tsunami" narrative that dominated headlines for the past two years is aging fast - especially if we look at long-term trends (see my previous newsletter)

Even in a weak demand environment, when listings fall, the market mechanically tightens. We're not heading into a frenzy. But a market that goes from oversupplied to merely well-supplied feels very different to buyers on the ground — and headlines shift before the data confirms it.

What This Doesn't Mean

This is not a call that prices are about to take off. They're not.

The macro backdrop is genuinely difficult. Canada has shed 112,000 jobs in the first four months of 2026 — worst stretch since the pandemic. Full-time employment is down 156,000 over just three months. Unemployment is at 6.9%.

Consumer insolvencies just hit a record high in February.

Credit card loss rates are at a decade high. Power of sale listings in Toronto are at their highest share of new listings ever recorded, and those distressed sales reset comps lower.

There will likely be more near-term price softness. Anyone telling you the bottom is definitively in is getting ahead of the data.

What This Does Mean

Sentiment right now is more negative than the data justifies — and that gap matters.

The Toronto MLS HPI was flat in April. First flat reading in over a year. Active inventory may have peaked. Listings are falling. The FTHB cohort is the right size and the right age to drive a recovery, and they're starting to move.

In my opinion, we're probably closer to a bottom than most people think — particularly for single-family homes in the GTA. Not a V-shaped recovery. Not prices screaming back to 2022 levels. But the period of meaningful decline is likely behind us, and the next 12–24 months look more like stabilization than continued deterioration.

The buyers who move before the headlines confirm the turn are the ones who look back at this window and understand what they were looking at.

If you're sitting on a down payment and trying to figure out whether now makes sense — let's actually run the numbers on your situation. That's exactly what I'm here for.

Austin Yeh is a Smith Manoeuvre Certified Professional and independent mortgage agent based in Toronto, funding mortgages across Canada. He specializes in advanced mortgage strategies for high-income earners, real estate investors, and self-employed borrowers.

Lender features and policies are subject to change. Always verify current product details directly with the lender or through an SMCP-certified mortgage broker. This article is for educational purposes and does not constitute financial or mortgage advice.