The jobs report was worse than it looks

The April jobs report dropped this morning and it was bad — worse than anyone expected.

Canada shed 18,000 jobs. Economists were forecasting a gain of 15,000. That's a 33,000-job swing in the wrong direction.

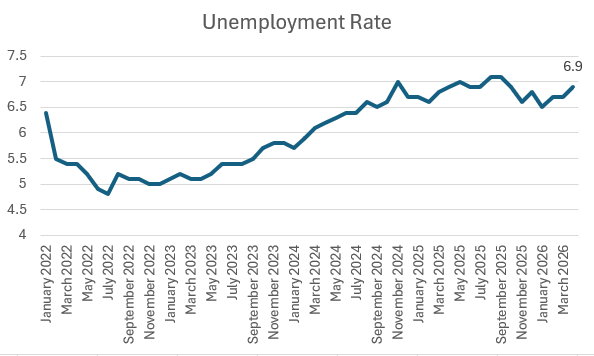

The unemployment rate climbed to 6.9%, its highest level in six months.

But the headline number is actually understating how weak things are. Let me walk you through why

The real unemployment picture is uglier than 6.9%.

The official unemployment rate only counts people actively searching for work. The moment someone gives up looking, they disappear from the stat entirely.

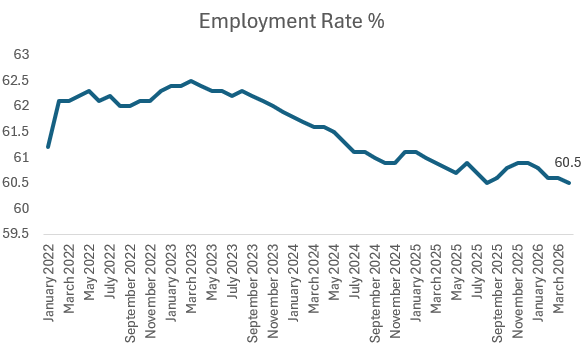

A better measure is the employment rate — the share of the total population that actually has a job. That fell to 60.5% in April, matching its lowest point since August 2025, and is down 0.3 percentage points year-over-year. Fewer Canadians are working as a share of the population, full stop.

Then there's long-term unemployment — people who've been searching for 27 weeks or more. That sits at 22.5%, significantly above the pre-pandemic average of 17.1%. Nearly 1 in 4 unemployed Canadians has been job hunting for over six months with nothing to show for it. That's not a temporary blip.

Full-time jobs are collapsing. Part-time is filling the gap.

This is the part most people miss.

Canada lost 47,000 full-time jobs in April while part-time employment rose by 29,000. Over the first four months of 2026, full-time work has fallen by 111,000.

The economy isn't just shedding jobs — it's replacing stable, full-time income with part-time hours. Someone who went from a 40-hour salaried position to a 15-hour shift job still counts as "employed" in the data. The unemployment rate never captures that downgrade.

Even the wage growth number is misleading.

The headline says wages grew 4.5% year-over-year. Sounds decent.

But StatsCan essentially footnotes their own number — once you control for the composition of who's actually working, real wage growth is 3.4%. The headline looks inflated because lower-paid, shorter-tenure workers are leaving the workforce faster, which mathematically pulls the average up. It's not that people are getting bigger raises. It's a statistical illusion.

The Bank of Canada looks at the composition-adjusted figure, not the headline.

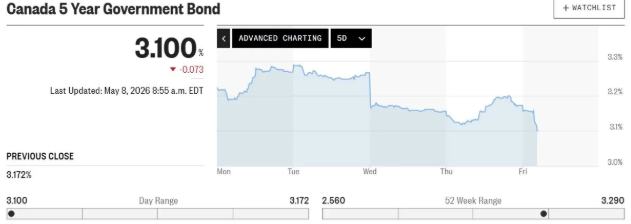

What the bond market is telling us.

The 5-year Government of Canada bond yield dropped on today's data — and it had already been falling earlier this week on reports of progress in US-Iran peace negotiations, which would ease energy price pressure (but this is also volatile in itself). At 3.100%, yields are still elevated, but fortunately there's been some relief. Markets are volatile and will continue to be so.

What today's report does is make it significantly harder for the Bank of Canada to justify raising rates into a deteriorating labour market. Higher rates in a fragile economy accelerate the damage. The Bank knows this.

The situation remains uncertain — it always does. But what we know today is that the labour market is weaker than the headline suggests, wage pressures are overstated, and bond yields are responding.

Having flexibility, understanding your goals, and focusing on strategy and what you can actually control matters more than ever right now.

If you have a refinance, renewal, or purchase coming up — let's talk.

Austin Yeh is a Smith Manoeuvre Certified Professional and independent mortgage agent based in Toronto, funding mortgages across Canada. He specializes in advanced mortgage strategies for high-income earners, real estate investors, and self-employed borrowers.

Lender features and policies are subject to change. Always verify current product details directly with the lender or through an SMCP-certified mortgage broker. This article is for educational purposes and does not constitute financial or mortgage advice.