Cash Damming on a Cash Flow Negative Property: Here’s Why It Still Works

One of the most common objections I hear about cash damming is this:

“My rental is cash flow negative. I’m already losing money every month. How would this strategy work for me?”

It’s a fair question. And the answer surprises most people.

Cash damming works just as well on a cash flow negative property as it does on a breakeven or positive one. In fact, the mechanics are almost identical — because the money you’re already spending out of pocket doesn’t disappear. It just gets rerouted.

Here’s what that actually looks like.

The Problem Most Investors Think They Have

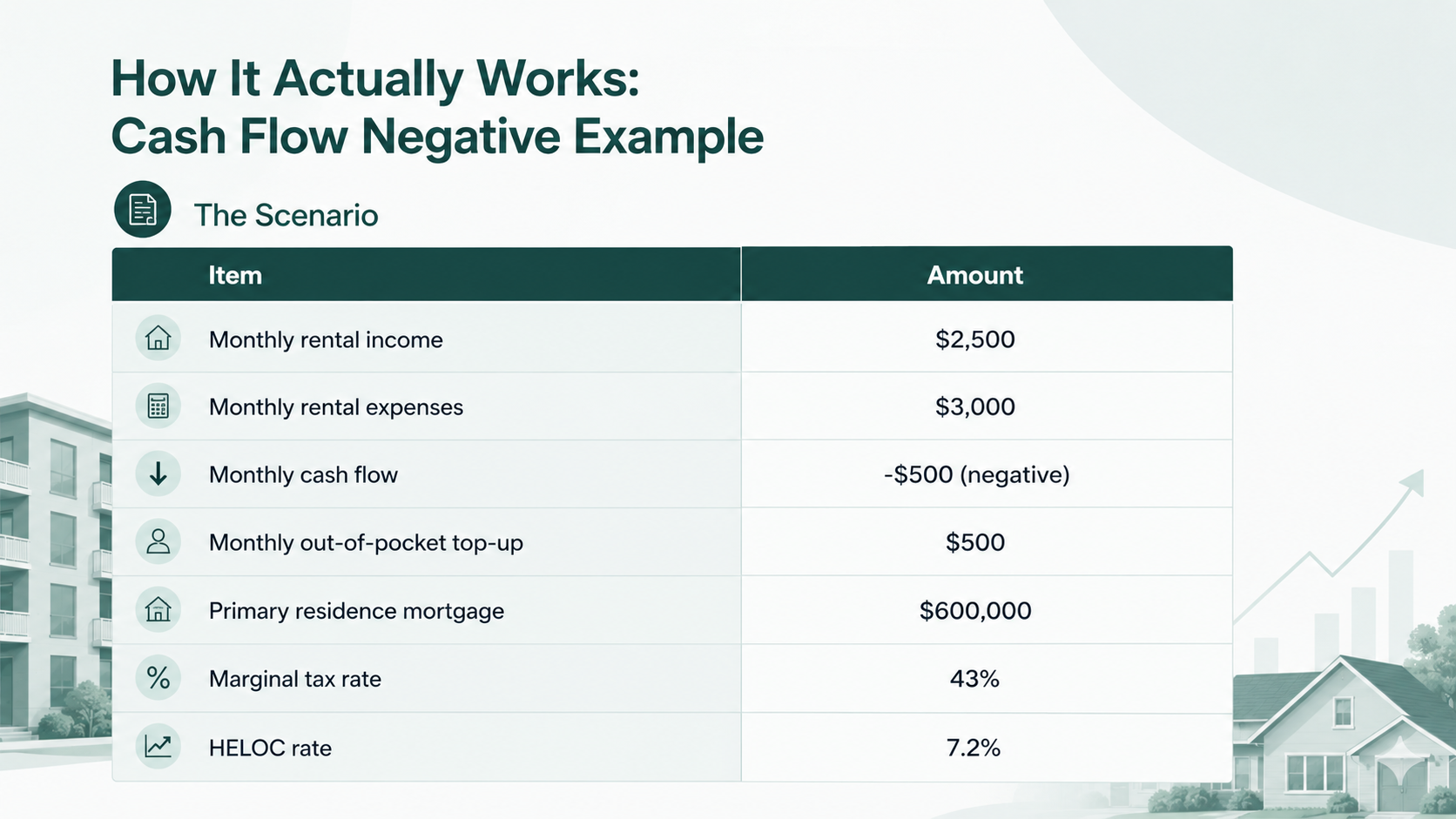

When a rental property is cash flow negative, the investor is topping up out of pocket every month. If rent is $2,500 and total expenses are $3,000, you’re contributing $500 per month from your personal funds just to keep the property running.

Most investors see that $500 as dead money. It’s gone. It covers expenses, produces no deduction beyond what already exists, and doesn’t move the needle on their personal mortgage.

What they’re missing is that cash damming doesn’t require positive cash flow. It requires cash flow — money moving in and out. Even on a negative property, that flow exists. You just need to route it correctly.

The Key Insight: Your Out-of-Pocket Cost Doesn’t Change

The Core Principle

Without cash damming, you are already spending money out of pocket every month to cover the shortfall on your rental.

Cash damming does not ask you to spend more money.

It asks you to route the money you are already spending differently — so that instead of covering expenses directly, it prepays your primary mortgage, while the HELOC covers the expenses instead.

The total dollars leaving your pocket remain exactly the same. What changes is the tax treatment of the debt those dollars create.

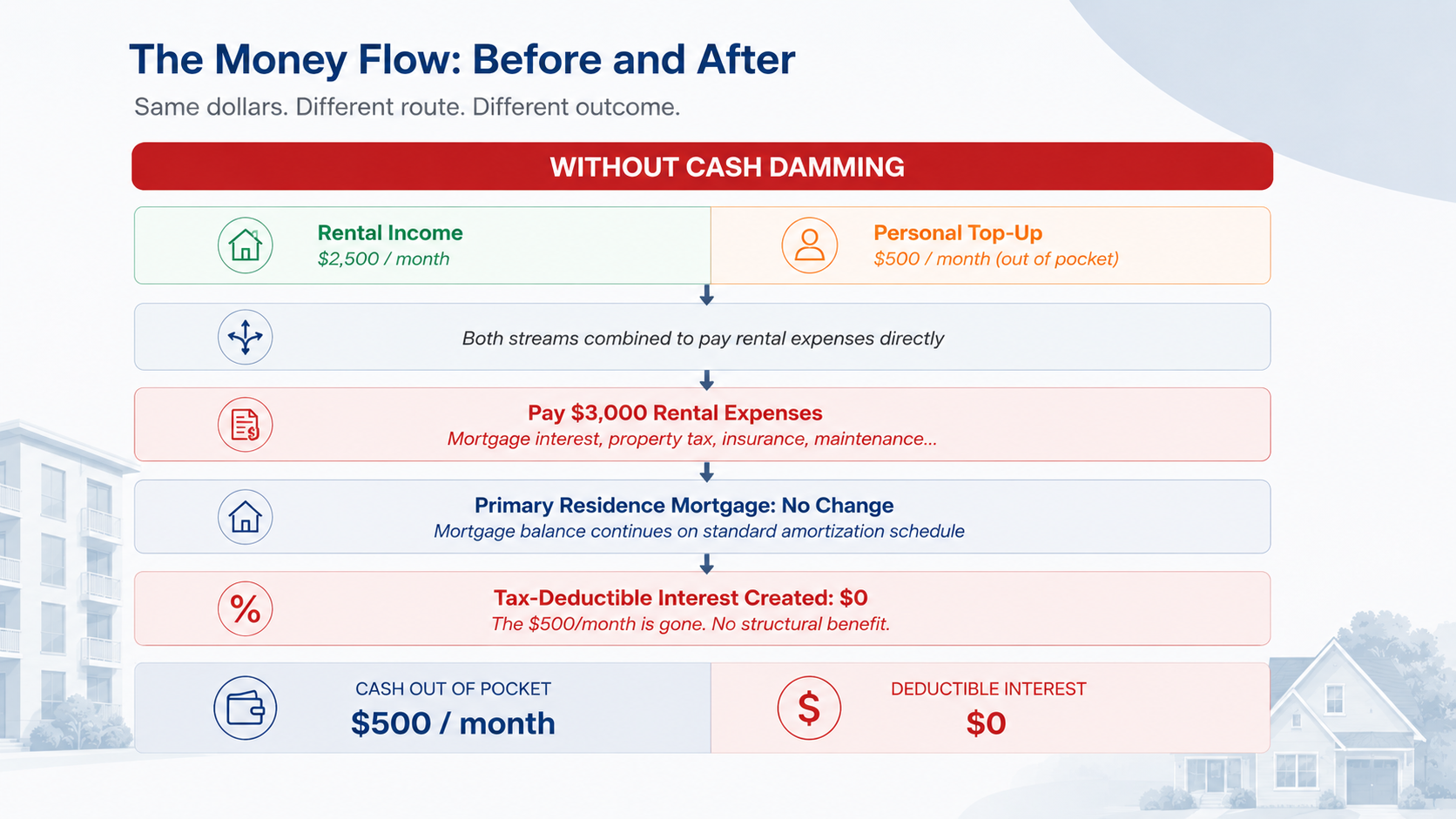

Without Cash Damming

Here is what the money flow looks like today:

Collect $2,500 in rent

Pull $500 from personal funds to cover the shortfall

Pay $3,000 in rental expenses directly

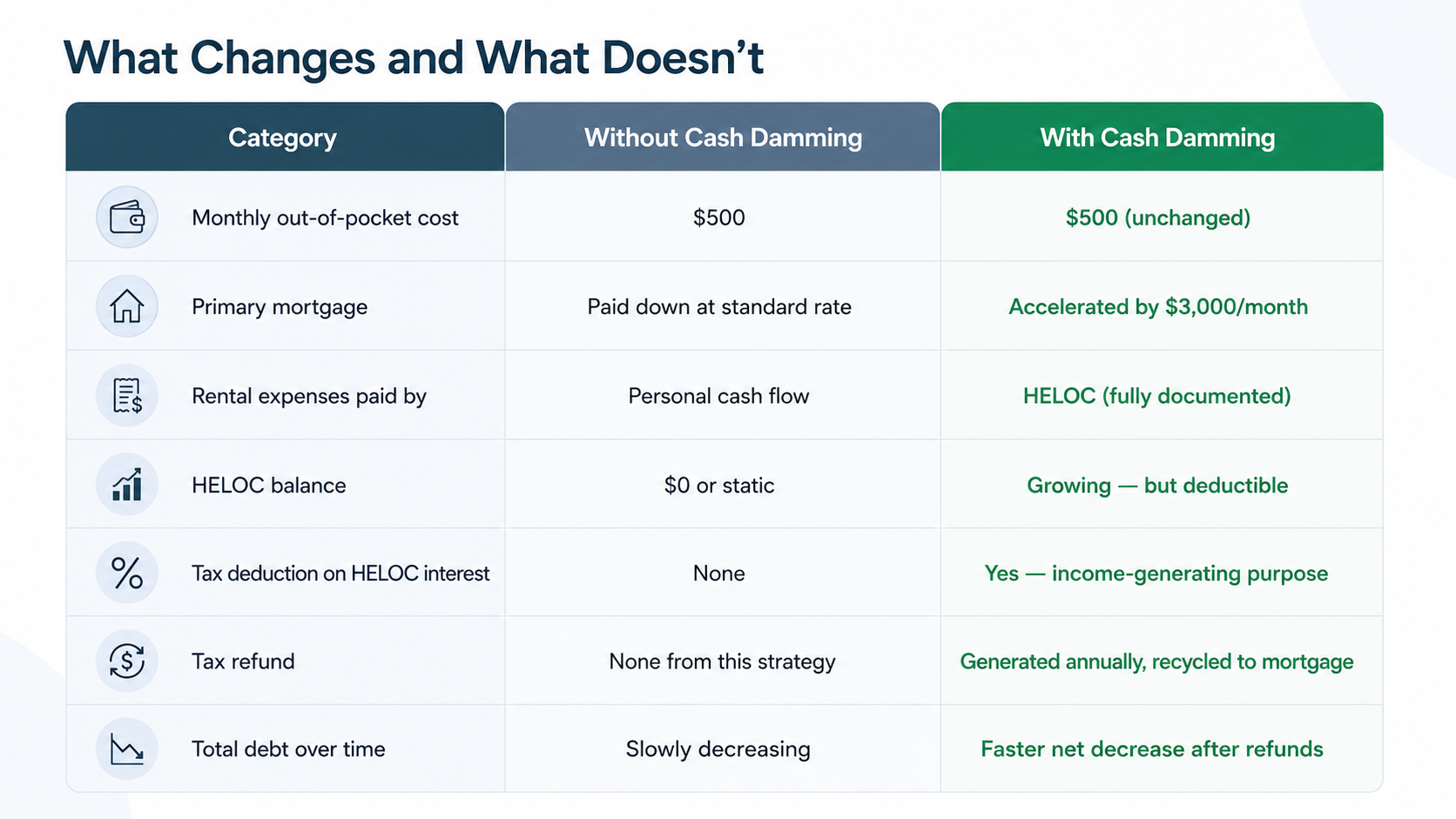

Net result: $0 deduction improvement, primary mortgage untouched, $500/month gone

You are spending $500 per month. The mortgage on your primary residence does not move. No additional tax deduction is created beyond the standard rental expense claims.

With Cash Damming

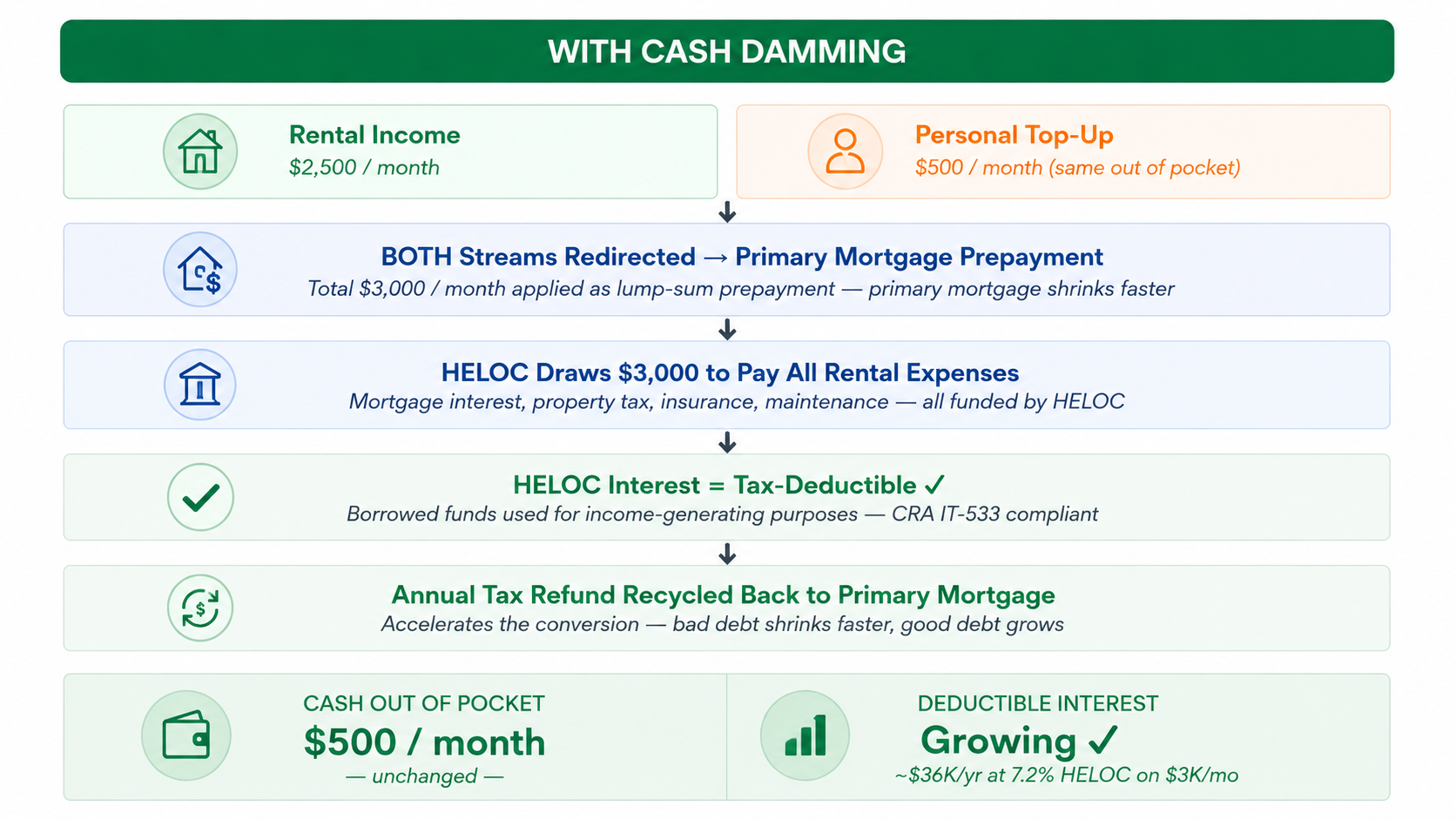

Here is what the money flow looks like with the strategy in place:

Collect $2,500 in rent — deposit into a dedicated business/rental income account

Add your $500 out-of-pocket top-up to the same account

Use the combined $3,000 to make a lump-sum prepayment on your primary residence mortgage

Draw $3,000 from the HELOC to pay all rental expenses

HELOC interest is now tax-deductible — because the borrowed funds were used for income-generating purposes

Annual tax refund gets applied back to the primary mortgage, accelerating the conversion

You are still spending $500 per month out of pocket. That has not changed.

But now, instead of that $500 disappearing into rental expenses with no structural benefit, it is prepaying your primary mortgage — and the HELOC is building a growing pile of tax-deductible debt in its place.

The Critical Takeaway

The $500/month you were already spending does not increase.

It does not decrease.

It just starts doing two jobs instead of one:

1. Prepaying your primary mortgage (combined with the rent)

2. Creating the mechanism for tax-deductible HELOC interest

The only thing that changes is where the money flows — and what it produces in return.

The One Requirement That Doesn’t Change

Whether the property is cash flow positive, breakeven, or negative, the CRA compliance requirements are identical.

Keep rental income and HELOC draw accounts completely separate

Document every HELOC withdrawal tied to a specific eligible rental expense

Never use the HELOC for personal spending — a single personal transaction can unwind the entire deductibility trail

Maintain records for a minimum of six years

Use a re-advanceable mortgage product that allows lump-sum prepayments and dollar-for-dollar HELOC re-advancement

The tracing requirement does not get easier or harder because the property is negative cash flow. It is the same standard. Execution is everything.

Who This Is For

This version of cash damming is particularly well-suited to:

Investors who bought in high-priced markets (Toronto, Vancouver) where negative cash flow is common

Long-term hold investors who are carrying properties at a short-term loss in exchange for appreciation

High-income earners in 40%+ tax brackets where the deduction creates meaningful annual refunds

Investors looking to make their existing out-of-pocket contributions work harder without spending an additional dollar

If you are already topping up a rental every month and accepting that as the cost of the investment, this strategy converts that cost into a structural wealth-building mechanism. The money was leaving your account either way. The question is whether it leaves with any benefit attached.

⚠️ Do Not Attempt Cash Damming Without Professional Guidance

Cash damming on a negative cash flow property involves the same CRA tracing requirements as any other version of the strategy.

The mortgage product must support lump-sum prepayments and dollar-for-dollar HELOC re-advancement. Not all lenders offer this. Choosing the wrong product makes the strategy impossible to execute correctly.

Speak with a qualified mortgage professional before implementing. This is not a DIY strategy.

⚠️ Legal / Tax / Financial Disclaimer

This article is for educational purposes only. Nothing in this article constitutes financial advice, mortgage advice, tax advice, or legal advice. Cash damming is a highly technical strategy that requires a properly structured re-advanceable mortgage, strict CRA tracing compliance, and coordination with qualified professionals. Do not attempt to implement this on your own. Always consult a qualified mortgage agent and tax advisor before taking any action.

Austin Yeh is a Smith Manoeuvre Certified Professional and independent mortgage agent based in Toronto, funding mortgages across Canada. He specializes in advanced mortgage strategies for high-income earners, real estate investors, and self-employed borrowers.

Lender features and policies are subject to change. Always verify current product details directly with the lender or through an SMCP-certified mortgage broker. This article is for educational purposes and does not constitute financial or mortgage advice.