Should I Cash Dam My Airbnb? (Probably Not — Here’s Why)

It’s a question I get asked more than you’d expect.

Short-term rental operators tend to be entrepreneurially-minded. They’re already optimizing their property, their pricing, their reviews. It makes sense that they’d ask whether cash damming — a strategy that can convert non-deductible mortgage debt into tax-deductible investment debt — applies to them too.

The short answer: technically, it is possible. Practically, it is generally not recommended — and the reason comes down to how the CRA treats short-term rental income, how that affects expense deductibility, and how much documentation is required to defend any deduction you claim.

This article breaks down why short-term rentals create problems for cash damming, what rental structure works better, and what the tracking burden actually looks like if you try anyway.

A Quick Recap: Why Rental Type Matters for Cash Damming

Cash damming works because borrowed HELOC funds are used to pay eligible rental expenses. The CRA allows interest deductibility on money borrowed to earn income from a property.

The critical word is “earn.” The CRA does not allow deductions across the full year simply because a property exists or is listed. It allows deductions proportional to the period the property is actually being used to earn income. For a long-term rental with a signed lease, that is straightforward. For an Airbnb, it is not.

How the CRA Defines Short-Term Rentals

For GST/HST purposes, the CRA generally defines a short-term rental as any accommodation rented for less than 30 consecutive days to the same occupant.

Rentals of 30 consecutive days or more to the same occupant are typically treated as long-term residential rentals, which are exempt from GST/HST.

For income tax and expense deductibility purposes, the CRA looks at actual eligible-use days — not simply whether the listing was active or the property was available. Occupied days and provable maintenance or cleaning days tied directly to rental activity are generally accepted. Vacant available days are typically not.

Important: This is a general framework based on CRA guidance and anecdotal conversations with Smith Manoeuvre-certified accountants. Tax law is complex and can change. Always speak with a qualified accountant before drawing conclusions about your specific situation.

What this means practically: if your Airbnb earned income on 110 nights and you can document 15 days of cleaning and maintenance, the CRA will typically consider roughly 125 days out of 365 as eligible rental days — about 34%. Your deductible expenses, and by extension your deductible HELOC interest, are limited to that proportion.

You cannot borrow 100% of annual expenses through the HELOC and claim full deductibility on that interest. The math only works on the eligible portion. The rest is personal, non-deductible, and must be separated cleanly — which is where the headaches begin.

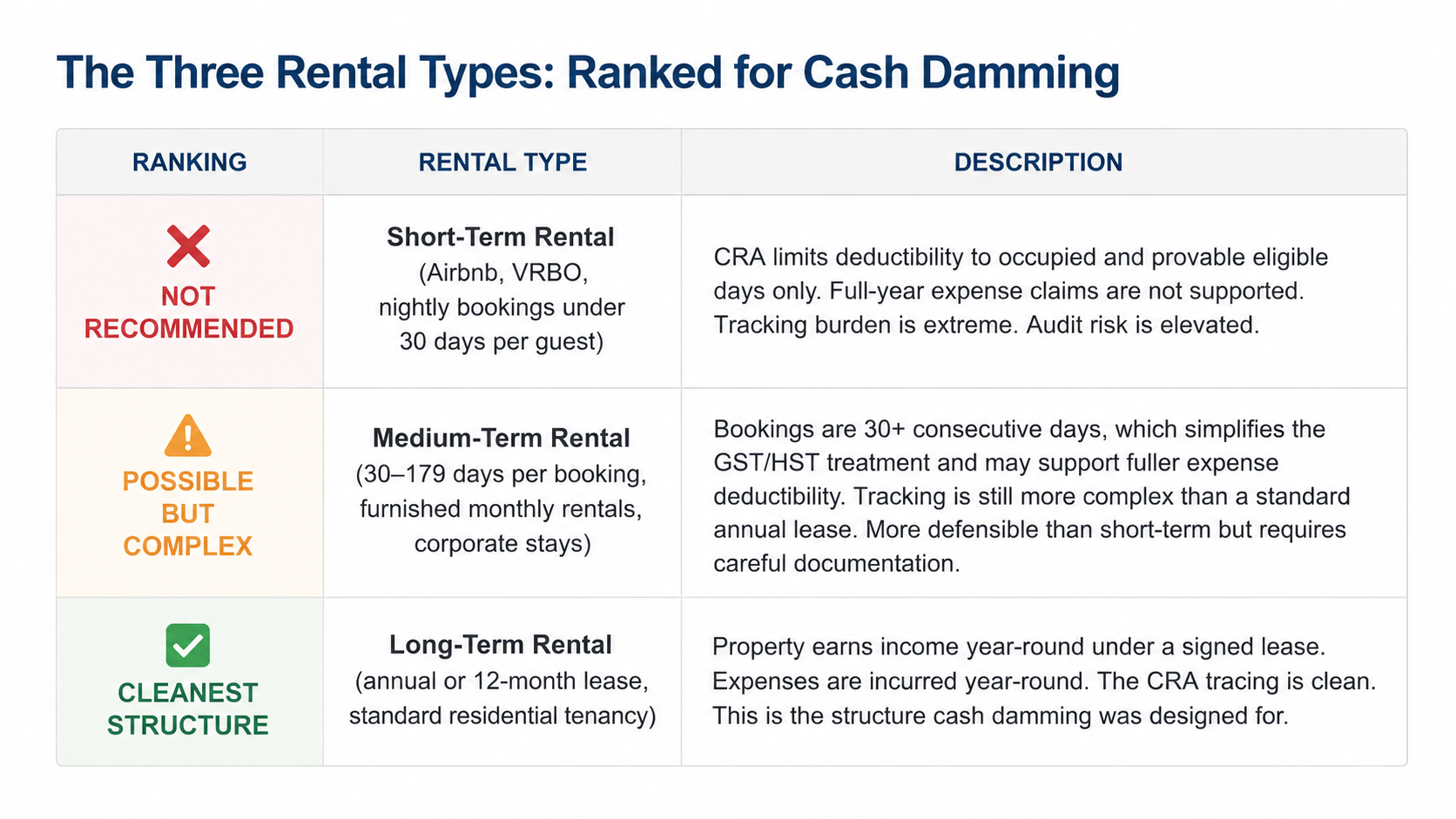

Short-Term Rentals: Why It Creates Problems

1. Deductibility Is Partial by Default

With a long-term rental, you can generally claim 100% of eligible rental expenses because the property is rented 100% of the time. With an Airbnb, you can only claim expenses proportional to eligible-use days. If that number is 35%, your HELOC interest deduction is 35% of what you borrowed — assuming your documentation is flawless.

This breaks the core cash damming structure, which relies on a clean one-to-one trace: 100% of HELOC funds go to 100% deductible expenses. Partial deductibility means partial tracing, which means splitting every HELOC draw between deductible and non-deductible portions and documenting every dollar separately.

2. Personal Use Days Kill the Deduction Entirely

If you use your Airbnb personally — even occasionally — those days are not eligible. Any expenses tied to personal-use periods are not deductible. Mixed-use properties require even more careful allocation, and commingling personal and rental HELOC draws is one of the fastest ways to lose the entire deduction trail.

3. The CRA Eligible-Use Test Is Narrow

The CRA will typically accept occupied days and provable maintenance or cleaning days directly tied to rental activity. It will not accept:

Days the property was listed but vacant

Days the property was blocked off for personal reasons

Speculative availability — “it could have been rented” is not a deductible day

In a typical Airbnb scenario with 100–150 booked nights per year, the eligible-use percentage often falls between 30% and 50% of the year. That ceiling limits how much deductible HELOC debt you can legitimately build, and how quickly the cash damming conversion can happen.

4. Seasonality Creates Uneven Cash Flow

Cash damming works best with consistent, predictable cash flow — so the prepayment and HELOC draw cycle runs smoothly month to month. Short-term rentals are inherently seasonal. Revenue spikes in summer, drops in winter. Expenses do not move the same way. That inconsistency makes the strategy harder to execute, harder to document, and harder to defend.

Medium-Term Rentals: Better, But Not Clean

A medium-term rental — typically defined as bookings of 30 consecutive days or more — avoids some of the short-term rental problems. Because each booking is 30+ days with the same occupant, the property looks more like a residential rental in the CRA’s eyes.

The eligible-use calculation is simpler. If the unit is occupied continuously from March through October under a series of monthly bookings, that’s eight months of documented rental income — roughly 65–70% of the year. That is a much stronger basis for expense deductibility than a typical Airbnb with 120 booked nights.

Cash damming is more defensible here. But it is still not as clean as a long-term lease, because you still need to document each booking period and calculate the eligible-use fraction annually. If there are gaps between bookings, those gaps are non-eligible. If you use the property personally between tenants, that complicates the allocation further.

Medium-term rentals sit in a middle ground: workable with the right structure and documentation, but requiring more ongoing attention than a standard annual lease.

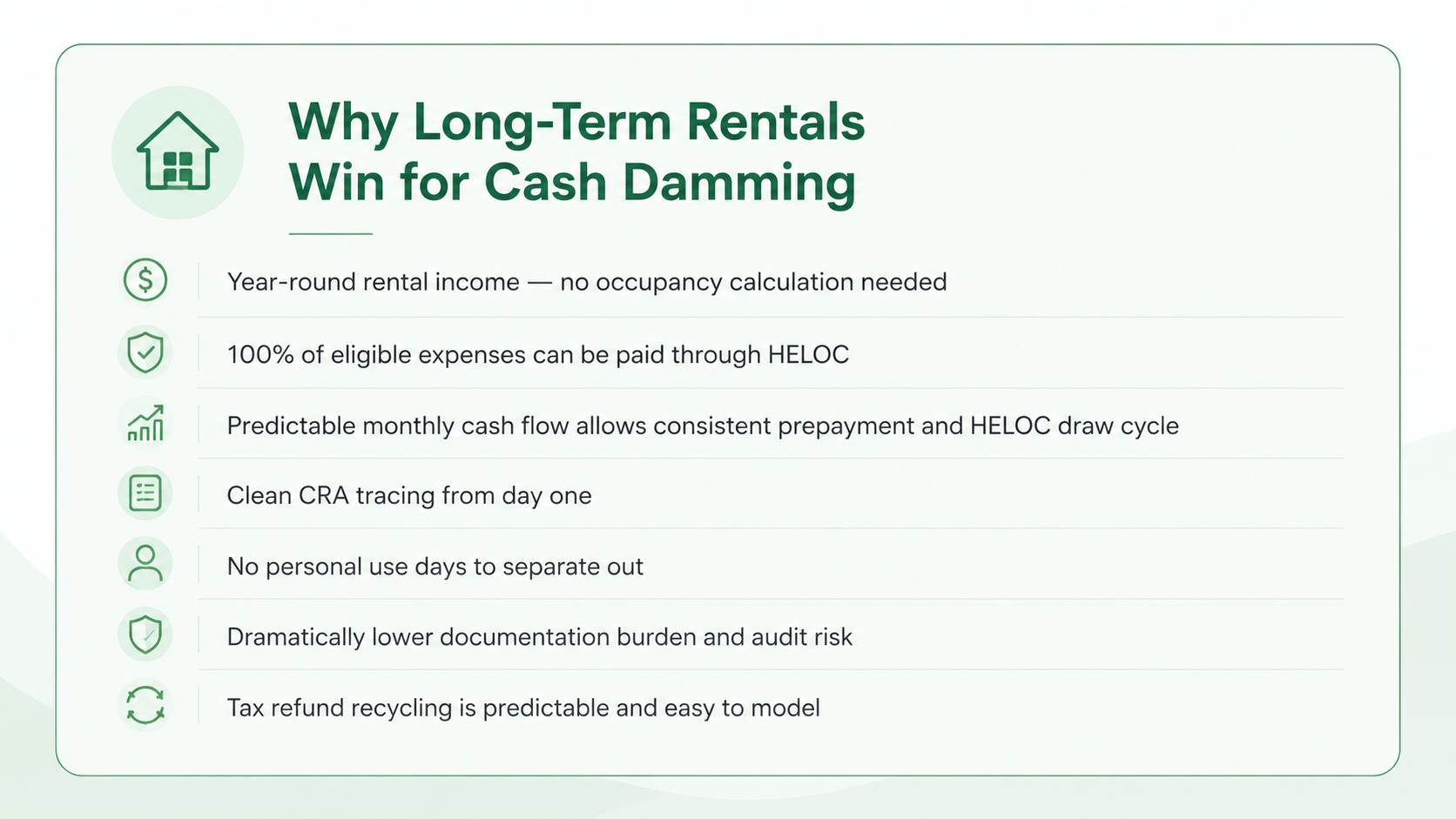

Long-Term Rentals: The Clean Structure

A property on a standard annual or 12-month lease is the environment cash damming was built for.

The tenant pays rent every month. You pay expenses every month. The eligible-use period is effectively 100% of the year. There are no occupancy calculations to run, no eligible-use fractions to determine, and no partial HELOC draws to allocate. The trace from borrowed HELOC funds to income-generating rental expenses is clean, consistent, and easy to document.

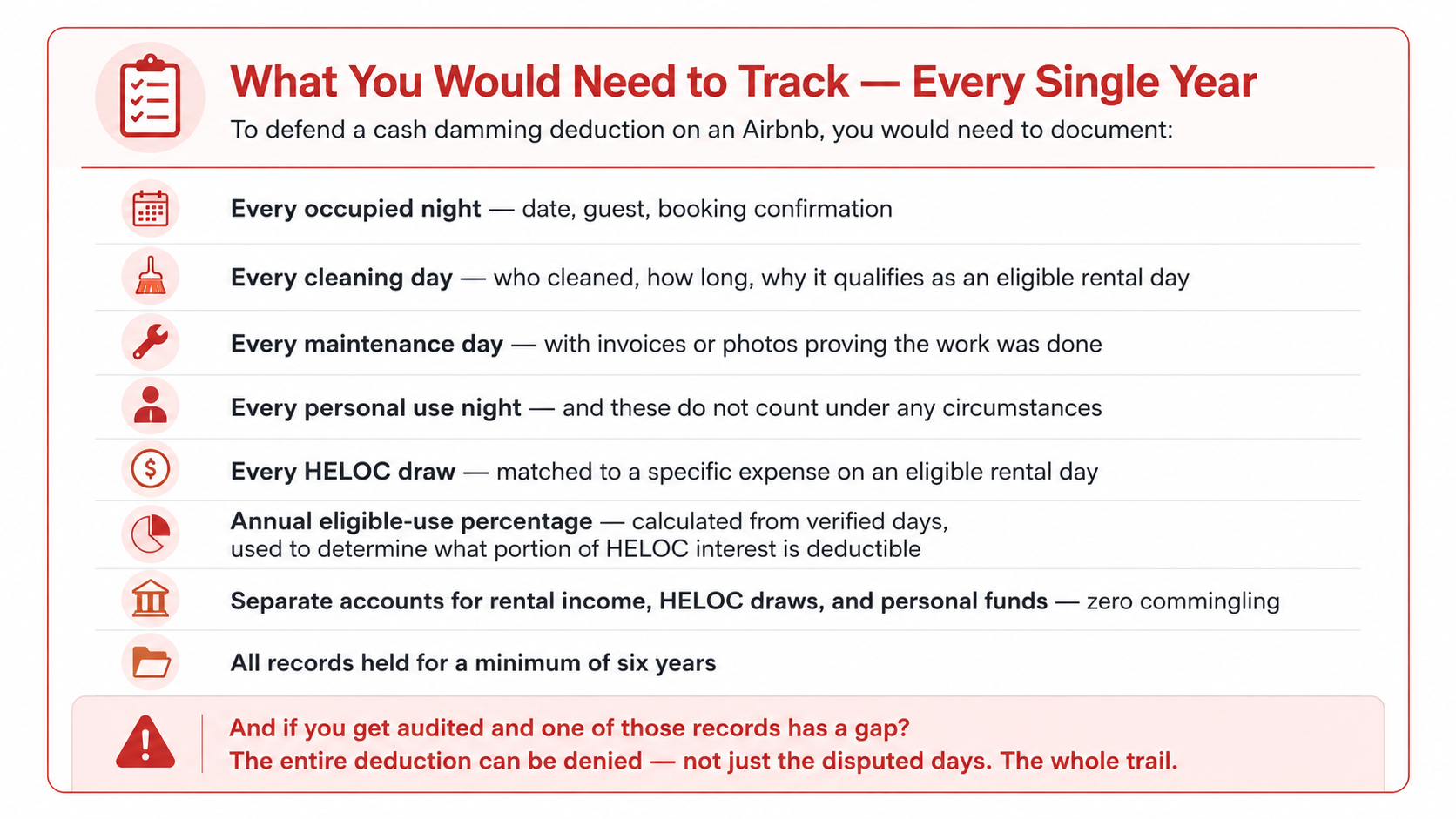

The Tracking Nightmare: What Cash Damming on an Airbnb Actually Requires

Let’s be specific about what you are signing up for if you try to cash dam an Airbnb.

This is not hypothetical. This is what a CRA auditor would ask for. And unlike a long-term rental where the documentation is a lease, a rent payment history, and a HELOC statement, the Airbnb version requires ongoing manual tracking of every use-day category for the life of the strategy — potentially a decade or more.

Most investors who attempt this underestimate the administrative burden until the first year-end reconciliation. By that point, records are incomplete, accounts have been commingled, and the deduction is already at risk.

So Should You Cash Dam Your Airbnb?

Cash damming on an Airbnb is not impossible. But the combination of partial deductibility, unpredictable cash flow, high documentation requirements, and elevated CRA scrutiny makes it a poor fit for most investors.

If you are open to converting the property to a medium or long-term rental, or if you are deciding how to structure a new acquisition, that is a conversation worth having before you commit to a rental model that limits your financing options.

⚠️ Legal / Tax / Financial Disclaimer

This article is for educational purposes only. Nothing in this article constitutes financial advice, mortgage advice, tax advice, or legal advice. Cash damming is a highly technical strategy that requires a properly structured re-advanceable mortgage, strict CRA tracing compliance, and coordination with qualified professionals. Do not attempt to implement this on your own. Always consult a qualified mortgage agent and tax advisor before taking any action.

Austin Yeh is a Smith Manoeuvre Certified Professional and independent mortgage agent based in Toronto, funding mortgages across Canada. He specializes in advanced mortgage strategies for high-income earners, real estate investors, and self-employed borrowers.

Lender features and policies are subject to change. Always verify current product details directly with the lender or through an SMCP-certified mortgage broker. This article is for educational purposes and does not constitute financial or mortgage advice.