Cash Damming vs Smith Manoeuvre in Canada: Which Strategy Fits You Best?

One of the most common misconceptions I hear is that cash damming and the Smith Manoeuvre are basically the same strategy.

It's easy to understand why people think that.

Both strategies use a HELOC. Both can gradually convert non-deductible debt into tax-deductible debt. Both come up constantly in conversations about mortgage optimization, tax efficiency, and long-term wealth building.

At a high level, they look remarkably similar.

In practice, they solve completely different problems — and that's where most investors get confused.

The question isn't whether both strategies can create tax-deductible debt. They can. The question is how that debt gets created, what risk you're taking on to create it, and what type of investor each one is actually built for.

Get that distinction right, and you'll know which strategy fits your situation in about five minutes. Get it wrong, and you'll end up implementing a strategy that technically works but doesn't match what you actually need.

The Short Answer

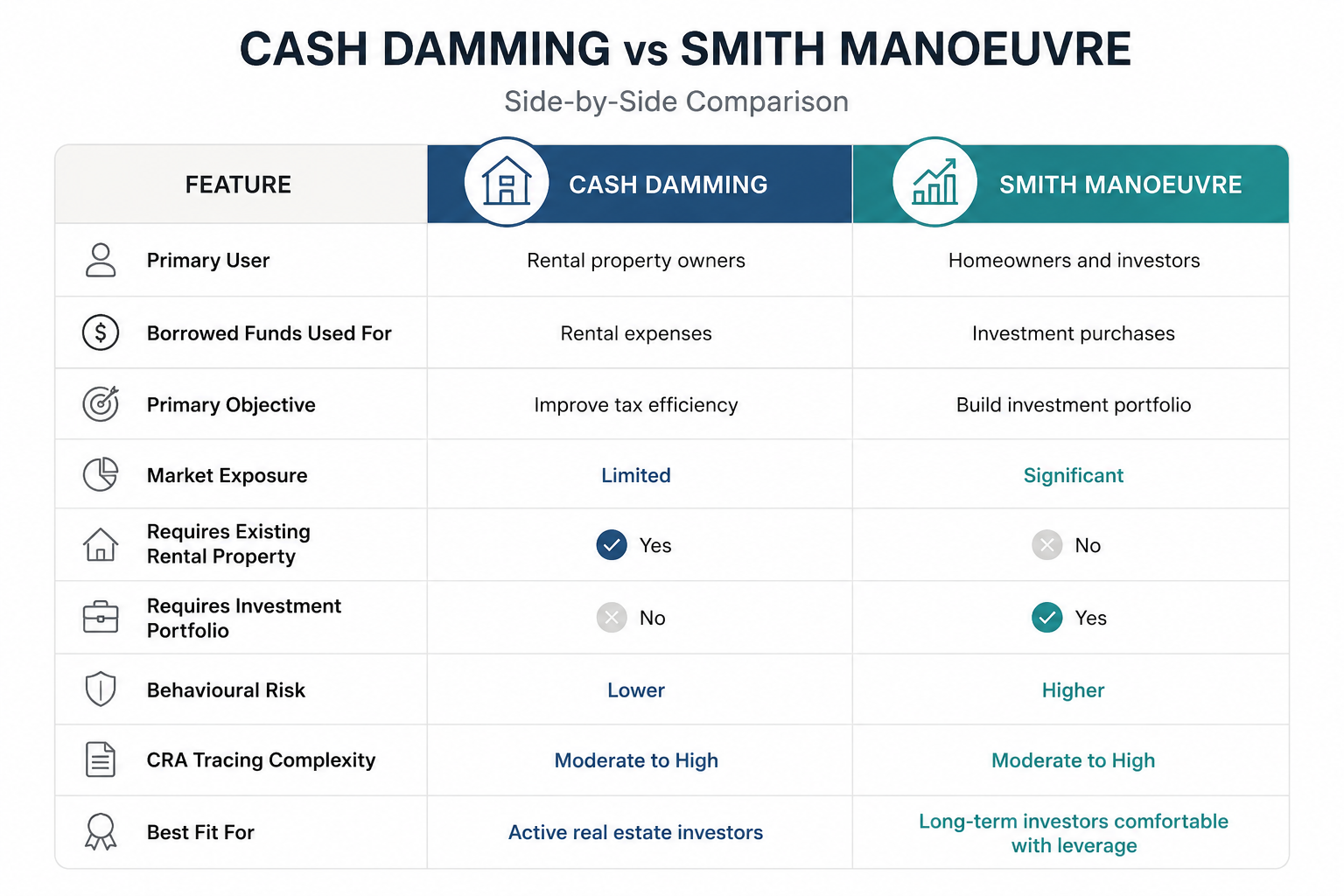

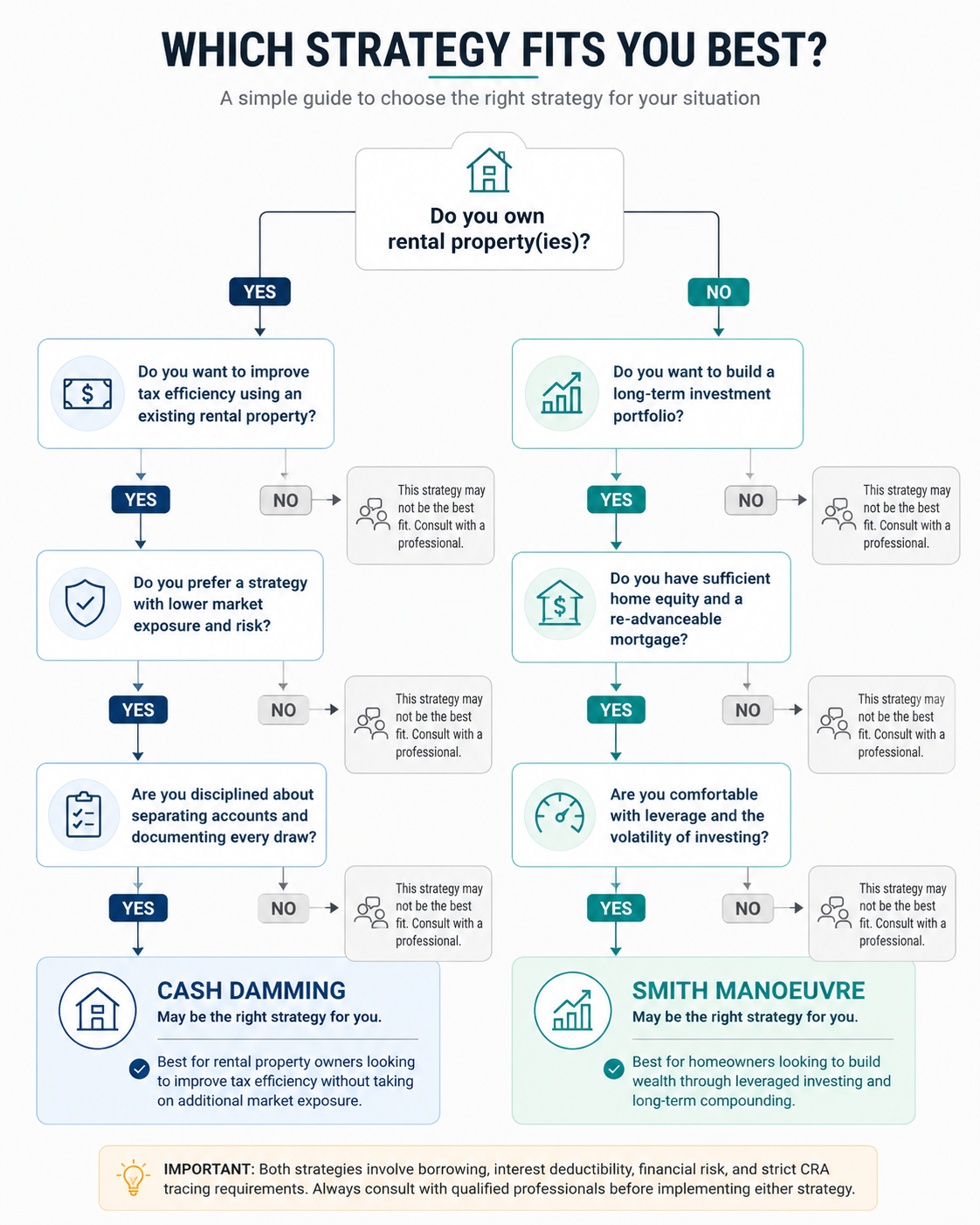

Cash damming is built for rental property owners. The Smith Manoeuvre is built for homeowners who want to build an investment portfolio using borrowed money.

Both strategies can improve tax efficiency, and both rely on the same general CRA principle that interest on borrowed money may be deductible when the funds are used for income-producing purposes, as set out in CRA Interpretation Bulletin IT-533. But they use completely different mechanisms to get there.

Cash damming restructures existing rental cash flow. The Smith Manoeuvre introduces investment leverage. That distinction changes the risk, the cash flow requirements, and the overall investor experience.

Why Investors Often Confuse the Two

The confusion usually starts with the HELOC.

Most investors learn that both strategies involve borrowing against home equity and that both can create deductible interest, and from there it's easy to assume they're just different flavours of the same idea. They're not.

What matters isn't the HELOC. What matters is what the borrowed money is being used for.

With cash damming, borrowed funds typically pay expenses that already exist inside a rental property business. With the Smith Manoeuvre, borrowed funds generally buy investments that didn't exist before. That sounds like a small distinction. It isn't — it changes how the entire strategy behaves.

What Is Cash Damming?

Cash damming is a Canadian tax strategy built primarily for rental property owners.

Instead of paying eligible rental expenses directly from rental income, the investor uses borrowed funds from a HELOC or re-advanceable mortgage to cover those expenses. The rental income that would normally pay those expenses is then redirected toward non-deductible personal debt — most commonly a primary residence mortgage.

Over time, more debt becomes tax-deductible, because the borrowed funds were used for income-generating purposes.

For most investors, the appeal is that cash damming works with expenses they're already paying. Property taxes already exist. Insurance already exists. Maintenance already exists. The rental property already exists.

The strategy isn't creating a new investment — it's restructuring cash flow around one that already exists. That's why most real estate investors treat cash damming as a tax-efficiency strategy first, not a wealth-building strategy.

What Is the Smith Manoeuvre?

The Smith Manoeuvre was developed by Canadian financial planner Fraser Smith. Like cash damming, the objective is to gradually convert non-deductible debt into tax-deductible debt — but the process is very different.

As mortgage principal is paid down, borrowing room becomes available through a re-advanceable mortgage structure. The homeowner re-borrows that available equity and invests it — typically into dividend-paying stocks, ETFs, mutual funds, private lending, investment real estate, or other income-producing assets.

Important: This only works with a re-advanceable mortgage that opens up dollar-for-dollar HELOC room as principal gets paid down. Not every lender offers this. If your current mortgage doesn't re-advance automatically, the Smith Manoeuvre isn't off the table — it just needs to be restructured first.

Unlike cash damming, the Smith Manoeuvre depends heavily on future investment performance. The investor is intentionally introducing leverage into a portfolio with the expectation that long-term returns will exceed the cost of borrowing. That creates the potential for greater wealth accumulation — and a very different kind of risk than cash damming carries.

The Difference Most Investors Miss

Most investors assume the difference between cash damming and the Smith Manoeuvre is simply rental expenses versus investments. That's technically true, but it isn't the distinction that matters most.

The biggest difference is where the risk comes from.

With cash damming, borrowed money is generally funding expenses that already exist inside an active rental business — you're restructuring cash flow that's already moving through your financial life. With the Smith Manoeuvre, borrowed money creates new investment exposure that didn't exist before — you're deliberately increasing leverage in pursuit of future returns.

One strategy reorganizes cash flow you already have. The other increases your exposure to investment markets. That difference shows up in liquidity risk, behavioural risk, volatility exposure, and how sensitive each strategy is to a bad month of cash flow.

It's why two strategies that look nearly identical on paper can feel completely different once real money is involved.

Cash Damming vs Smith Manoeuvre: Side-by-Side Comparison

What This Looks Like in Practice

Imagine a rental property generating $4,000 a month in rent, with $2,200 a month in expenses.

Without cash damming, a portion of that rent simply pays those expenses.

With cash damming, those same expenses get paid through the HELOC instead. The rental income that would have covered them is now redirected toward the primary residence mortgage.

The property hasn't changed. The expenses haven't changed. The rent hasn't changed. Only the route the money takes has changed — and that route is what creates the tax benefit.

Now compare that to the Smith Manoeuvre.

Imagine a homeowner with a $500,000 mortgage paying down $1,200 a month in principal. Under the Smith Manoeuvre, that $1,200 becomes new HELOC room the same month. The homeowner draws that $1,200 and invests it into a portfolio of dividend-paying stocks. The interest on that draw is now deductible, because the borrowed money was used to earn investment income.

The mortgage hasn't changed. The payment hasn't changed. What's new is $1,200 a month of investment exposure that didn't exist before — and a deduction that now depends on whether that portfolio earns more than the HELOC costs to carry.

That's the trade-off cash damming doesn't have. Cash damming's tax benefit doesn't depend on market performance. The Smith Manoeuvre's does.

The mechanics may sound similar. The experience is not.

CRA Compliance: What Both Strategies Require

Regardless of which strategy you use, the CRA requires a clear, defensible connection between the borrowed funds and the income-producing purpose they were used for. In practice, that means:

Keep the HELOC and your personal accounts completely separate — no commingling, ever.

Document every HELOC draw with a clear note tied to a specific rental expense (cash damming) or a specific investment purchase (Smith Manoeuvre).

Never use the HELOC for personal spending. A single personal transaction can compromise the entire deductibility trail.

Maintain all records for a minimum of six years.

Poor tracing is one of the fastest ways to lose interest deductibility on either strategy — and it's the most misunderstood part of both. The strategy itself is only half the equation. Execution is the other half.

Which Strategy Is Right for You?

Neither strategy is inherently better. They're built for different situations, and the right choice depends on your assets, your cash flow, your risk tolerance, and what you're actually trying to build.

The Bottom Line

Cash damming and the Smith Manoeuvre get grouped together because both use a HELOC and both can create tax-deductible debt. But they're not interchangeable.

Cash damming restructures existing rental cash flow. The Smith Manoeuvre introduces investment leverage.

One is a tax-efficiency strategy for rental property owners. The other is a leveraged investing strategy built to grow wealth through long-term compounding.

Knowing which one you're actually looking at is the first step. Knowing which one fits your numbers is the next — and that's not something you should guess at.

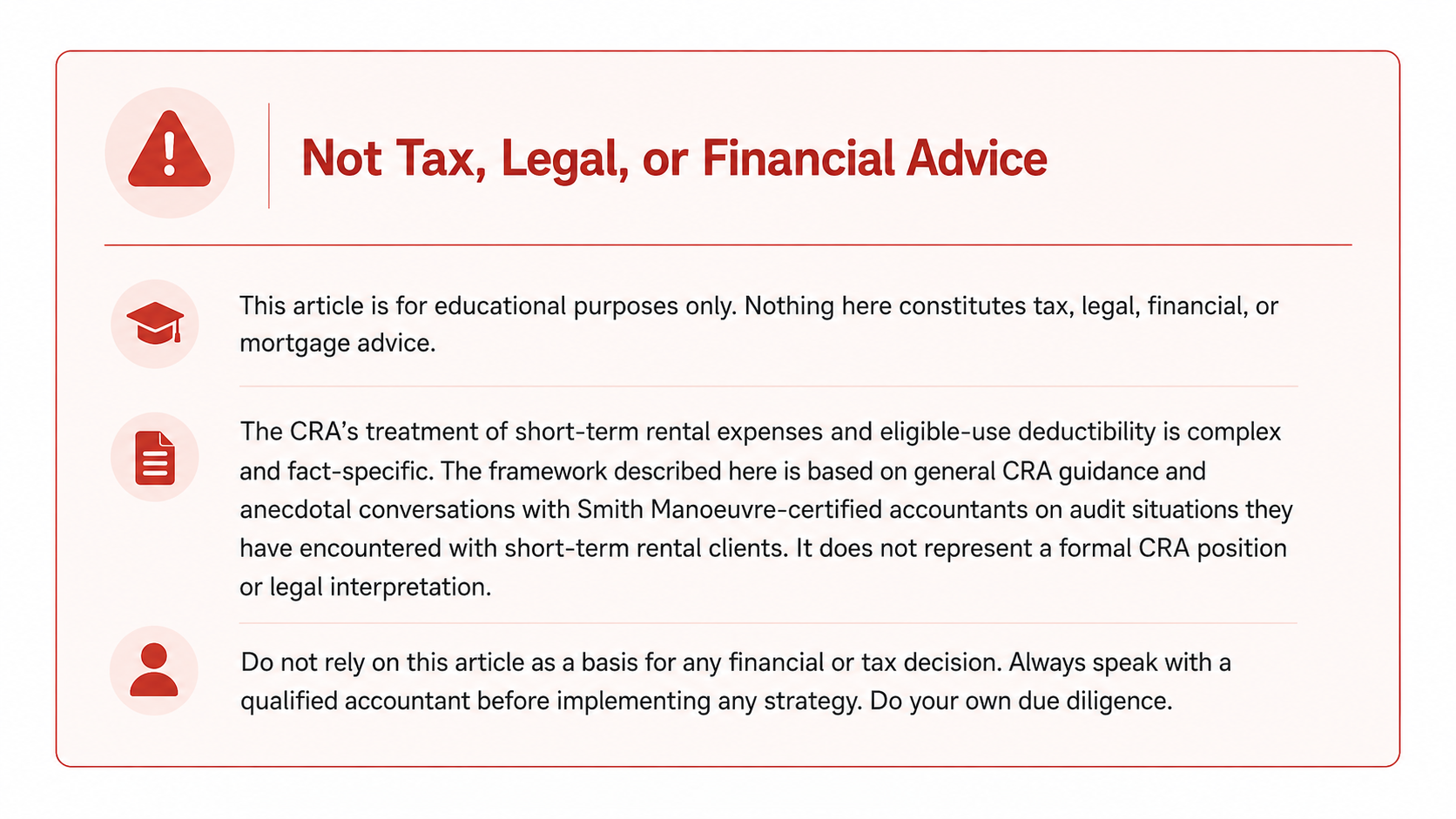

⚠️ Legal / Tax / Financial Disclaimer

This article is for educational purposes only. Nothing in this article constitutes financial advice, mortgage advice, tax advice, or legal advice. Cash damming is a highly technical strategy that requires a properly structured re-advanceable mortgage, strict CRA tracing compliance, and coordination with qualified professionals. Do not attempt to implement this on your own. Always consult a qualified mortgage agent and tax advisor before taking any action.

Austin Yeh is a Smith Manoeuvre Certified Professional and independent mortgage agent based in Toronto, funding mortgages across Canada. He specializes in advanced mortgage strategies for high-income earners, real estate investors, and self-employed borrowers.

Lender features and policies are subject to change. Always verify current product details directly with the lender or through an SMCP-certified mortgage broker. This article is for educational purposes and does not constitute financial or mortgage advice.