The Biggest Cash Damming Misconceptions in Canada

Cash damming has become one of the most discussed tax strategies among Canadian real estate investors.

It has also become one of the most misunderstood.

Spend enough time on social media, YouTube, or real estate forums and you will eventually see cash damming described as a mortgage hack, a tax loophole, or a shortcut to becoming mortgage-free faster.

None of those descriptions are accurate.

The reality is both simpler and more complicated. Cash damming is a legitimate debt restructuring strategy that can improve tax efficiency when implemented correctly. But it is also a strategy that depends on proper mortgage structure, clean bookkeeping, disciplined cash management, and strict CRA tracing requirements.

This is where most investors get into trouble. They focus on the tax deduction and ignore the structure required to create it.

Here are the most common misconceptions, and what actually matters when evaluating whether the strategy fits your situation.

1 Cash Damming Is a Tax Loophole

It isn't. It is a debt restructuring strategy built on established tax principles.

This is probably the most common misunderstanding.

Cash damming is not a tax loophole. The strategy is built on long-standing Canadian tax principles surrounding interest deductibility. In general, the CRA allows interest deductibility when borrowed money is used for the purpose of earning income from a business or property.

Cash damming does not create a new rule. It simply restructures how existing rental cash flow is used.

Instead of paying rental expenses directly from rental income, eligible expenses are paid using borrowed funds from a HELOC or re-advanceable mortgage. The rental income that would normally cover those expenses is then redirected toward reducing non-deductible personal debt.

The strategy itself is not controversial. The challenge is execution.

When investors mix personal spending with rental borrowing, lose documentation, or fail to maintain proper tracing, deductions can be challenged. That does not mean the strategy is illegal. It means the implementation failed.

2 A HELOC Automatically Creates Tax-Deductible Interest

The account doesn't matter. The use of funds does.

This is where many investors make their first major mistake.

A HELOC by itself does not create tax deductibility. What matters is how the borrowed funds are used.

The CRA focuses on the use of borrowed money, not the borrowing vehicle itself. If borrowed funds are used for an income-producing purpose, the interest may be deductible. If borrowed funds are used for personal consumption, the interest is not.

This distinction becomes critically important when investors begin mixing transactions. A HELOC used exclusively for rental expenses is relatively straightforward to trace. A HELOC used for rental expenses, personal renovations, vacations, and day-to-day spending becomes significantly more difficult to defend.

This is why experienced practitioners place so much emphasis on account separation and documentation. The deduction comes from the use of funds, not the HELOC itself.

3 Cash Damming Eliminates Debt

It changes the structure of debt. But it can also help you get mortgage-free faster.

Cash damming does not eliminate debt. It changes the structure of debt.

That distinction is one of the most important concepts for investors to understand. The strategy gradually converts non-deductible debt into potentially deductible debt over time. What changes is the tax treatment of the debt, not the existence of the debt itself.

Many investors mistakenly focus on watching their personal mortgage balance decline while ignoring the growth of the deductible borrowing replacing it. The total debt often remains similar for years. The benefit comes from improving tax efficiency and accelerating the conversion of debt from one category to another.

That said, cash damming can absolutely help you pay down debt and become mortgage-free faster. It happens in two stages.

Phase 1: Debt Conversion. You continue making your regular mortgage payments on your primary residence as normal. At the same time, cash damming is running alongside, which means rental income is prepaying your primary mortgage faster while the HELOC covers rental expenses. Every month, bad debt on your primary residence shrinks and is replaced by tax-deductible HELOC debt. The tax refund generated by the HELOC interest gets applied back to the primary mortgage, which accelerates the conversion further. This compounds. Depending on the rental income and mortgage size, this phase typically takes six to twelve years to complete, at which point your primary mortgage reaches zero.

Phase 2: Debt Paydown. Once the primary mortgage is gone, you have no more non-deductible debt. Only the HELOC remains. At this point, you redirect your former mortgage payment toward paying down the HELOC instead. You continue receiving annual tax refunds on the HELOC interest, and those refunds also go straight at the balance. Because the HELOC is fully deductible and you are making aggressive payments toward it, it typically gets paid off years ahead of schedule.

The result: you end up debt-free significantly earlier than if you had stayed on a standard mortgage amortization. Cash damming does not eliminate debt by itself. But it restructures debt in a way that, combined with tax refunds and disciplined repayment, can get you to zero faster than most conventional approaches.

4 Cash Damming Is Only for High-Income Investors

Income matters. Discipline matters more. But here is why the math favours higher brackets.

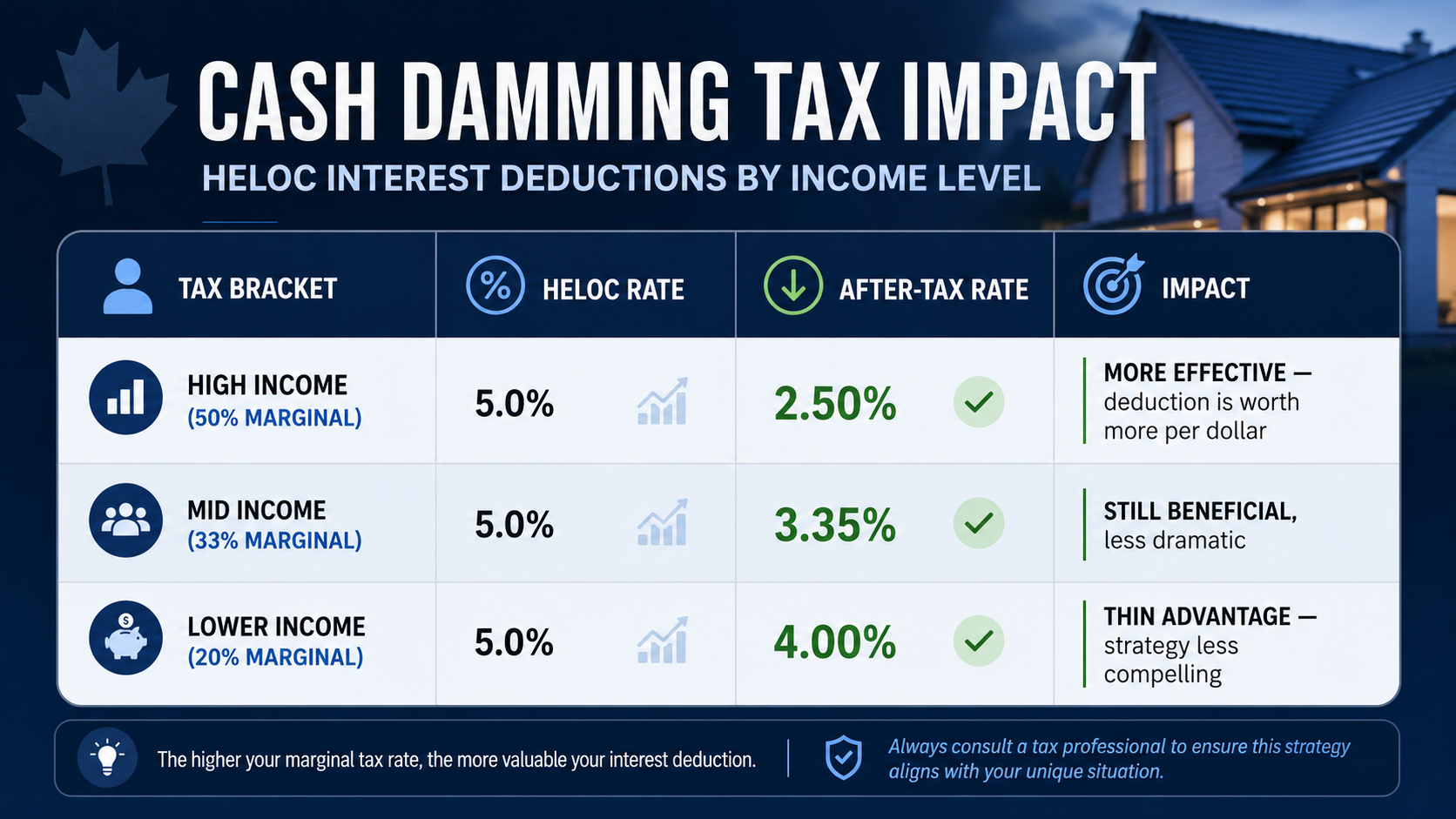

Higher-income earners often benefit more from cash damming because larger tax deductions generally create larger tax savings. Let's put actual numbers on why.

When you borrow through a HELOC for eligible rental expenses, the interest on that HELOC is tax-deductible. What that deduction is actually worth depends on your marginal tax rate.

If your HELOC rate is 5% and you are in a 50% marginal bracket, your after-tax borrowing cost is effectively 2.50%. That is an extraordinarily cheap way to fund income-producing expenses. For someone at a 20% bracket, the same 5% HELOC costs 4% after tax. Still a deduction, but the spread between what they are paying and what they would have paid without the strategy is much smaller.

This is why the strategy delivers more value at higher tax brackets. The deduction is worth proportionally more.

That said, what is not true is the idea that only high-income Canadians can implement the strategy. Many middle-income homeowners with stable employment, rental income, sufficient home equity, and strong financial habits may be structurally suitable candidates. Income matters. But discipline matters more.

The investors who tend to succeed with cash damming are usually not the investors with the highest incomes. They are often the investors with the strongest systems, the cleanest bookkeeping, and the most consistent financial behaviour.

4b Cash Damming Is Dangerous If Interest Rates Go Up

Actually, rising rates often make the strategy more advantageous for high-income earners.

This one is counterintuitive, and most people get it backwards.

The common concern goes like this: if HELOC rates rise, the interest cost on the strategy increases and the whole thing becomes more expensive. That is true in isolation. But it misses two things that matter more.

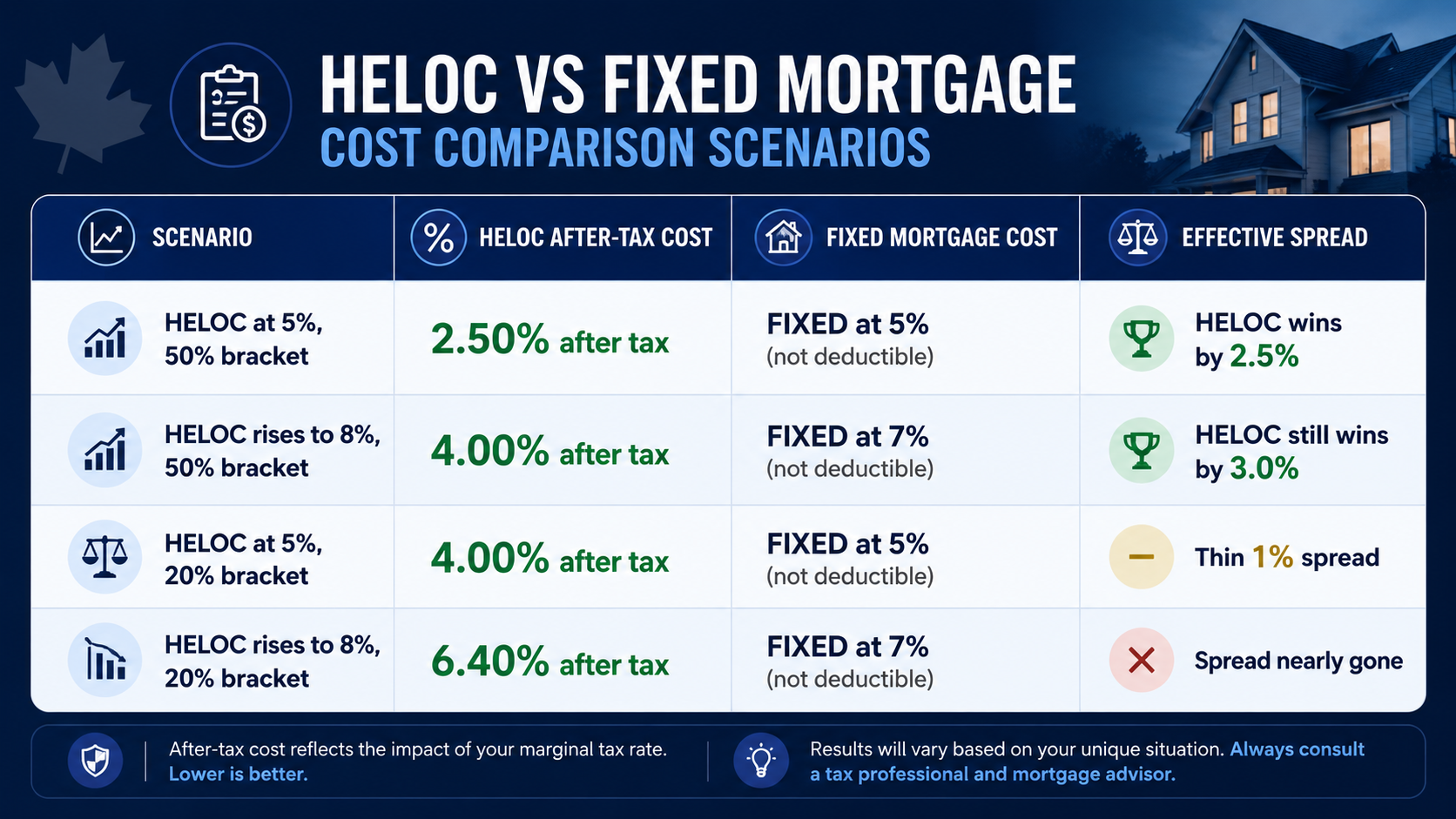

First, when rates rise across the board, fixed mortgage rates also rise. Your alternative to a deductible HELOC is a non-deductible fixed mortgage. In a rising rate environment, that fixed rate rises alongside everything else. So the comparison that matters is not the absolute HELOC cost, it is the after-tax HELOC cost versus the non-deductible fixed rate.

In the 50% marginal bracket scenario where HELOC rates have risen to 8%, the after-tax cost is 4%. The fixed mortgage rate in that same environment has likely risen to 7% or higher, and that rate is not deductible at all. You are borrowing at 4% effective after-tax cost versus 7% non-deductible. The spread in favour of cash damming has actually widened.

Second, the concern about rates going up dramatically assumes a scenario so extreme that the least of your worries would be your HELOC rate. If the Bank of Canada raises rates twelve times, interest rates rising is not the primary problem. Everything else is already in crisis. And even then, the math above still holds.

At lower tax brackets, rising rates do compress the advantage. Someone at a 20% marginal rate with a HELOC at 8% has an after-tax cost of 6.4%, which is not far from a 7% fixed rate. For lower-income investors, rising rates genuinely narrow the benefit.

For high-income earners, the opposite is true. A higher rate environment paired with a higher marginal tax bracket actually makes cash damming proportionally more valuable, not less. The deductibility shields you from a meaningful portion of the rate increase in a way that a non-deductible mortgage never can.

5 Cash Damming and the Smith Manoeuvre Are the Same Strategy

Both use a HELOC. The similarity mostly ends there.

This misconception comes up constantly. The confusion is understandable because both strategies involve a HELOC and both can gradually convert non-deductible debt into tax-deductible debt. At a high level, they can appear remarkably similar.

In practice, they are solving different problems.

Cash damming is primarily a tax-efficiency strategy for rental property owners. The Smith Manoeuvre is primarily a leveraged investing strategy. The difference may sound small. It isn't.

Applying the wrong strategy to your situation, or combining them without understanding the distinction, is one of the more common and expensive mistakes investors make.

6 CRA Rarely Looks at These Strategies

The CRA pays close attention to interest deductibility claims.

Many investors assume that if a deduction appears on a tax return, it will simply be accepted. That is not how tax compliance works.

The CRA pays close attention to interest deductibility claims, particularly when significant amounts are involved. The issue is not whether cash damming is allowed. The issue is whether the investor can support the deduction being claimed.

This is why documentation matters so much. Separate accounts, dedicated borrowing facilities, organized records, monthly reconciliations, and clean tracing are not optional administrative details. They are the evidence that supports the deduction.

The investors who navigate reviews and audits successfully are usually the investors who built strong systems long before they ever needed them.

The Misconception Behind Every Misconception

Most misunderstandings about cash damming come from the same place: investors focus on the tax deduction and ignore the structure.

The tax benefit is the outcome. The structure is what creates the outcome.

Without proper tracing, bookkeeping, mortgage design, and financial discipline, the strategy quickly becomes much harder to execute than many investors expect. This is why experienced investors spend less time talking about deductions and more time talking about process.

What Cash Damming Actually Does

At its core, cash damming is a debt restructuring strategy.

Rental income that would normally pay rental expenses is redirected toward non-deductible debt. Borrowed funds are used to pay eligible rental expenses, creating the potential for interest deductibility.

The objective is not free money. The objective is improving tax efficiency and optimizing the long-term structure of debt. Done correctly, it can also accelerate the path to becoming mortgage-free. But the structural discipline has to come first.

Final Thoughts

Cash damming is one of the most misunderstood strategies in Canadian real estate investing.

Some investors overhype it. Others avoid it because they misunderstand how it works. The reality sits somewhere in the middle.

When properly structured, cash damming can improve tax efficiency, strengthen cash flow flexibility, optimize debt structure over time, and help investors reach debt-free faster than conventional amortization. But it also requires discipline, documentation, clean tracing, and ongoing oversight.

The investors who tend to benefit most are not looking for shortcuts. They are looking for a structure that remains effective through multiple market cycles.

⚠️ Do Not Attempt Cash Damming Without Professional Guidance

Cash damming involves mortgage structuring, tax deductibility, leverage risk, CRA tracing requirements, and ongoing bookkeeping discipline. Mistakes in execution can invalidate deductions, create CRA reassessment exposure, increase financial stress, and compromise long-term strategy performance. Before implementing cash damming, speak with a qualified mortgage professional, an accountant experienced with CRA tracing requirements, and a tax advisor familiar with leveraged deductibility strategies.

Austin Yeh is a Smith Manoeuvre Certified Professional and independent mortgage agent based in Toronto, funding mortgages across Canada. He specializes in advanced mortgage strategies for high-income earners, real estate investors, and self-employed borrowers.

Lender features and policies are subject to change. Always verify current product details directly with the lender or through an SMCP-certified mortgage broker. This article is for educational purposes and does not constitute financial or mortgage advice.