The Bank of Canada meets in 16 days

Over 90% of markets are expecting no change. They're probably right.

But what does the rest of 2026 hold?

Firstly, the economy is weaker than the headlines suggest.

Canada lost over 109,000 jobs in the first two months of 2026. March added back 14,000, and markets were expecting more. But even that number is misleading — every single net job added in March was part-time work. The kinds of jobs people take when they can't find anything better.

The sectors actually growing were tradespeople and resource extraction. Meanwhile finance, insurance and real estate lost jobs. Manufacturing is down 44,000 positions year-over-year, a direct casualty of U.S. tariffs. Almost all of March's gains were carried by the Prairie provinces — and if you live and work in Ontario, the national headline is not your reality. Toronto's unemployment rate sits at 8.1%.

Normally this is exactly the environment where the Bank of Canada cuts rates. Lower rates, cheaper borrowing, people start spending and hiring again. That's how it's supposed to work.

But they can't right now. And that's the problem.

The Iran conflict changed everything.

The conflict has introduced a real risk of longer-term inflation through surging oil and energy prices. Here's what the Bank actually said — which most people missed:

"The Governing Council will look through the war's immediate impact on inflation."

"If energy prices come back down and we see more weakness in the economy, we can lower our policy rate."

In other words — they want to cut. The economy arguably needs it. But they're frozen until there's clarity on how the conflict and inflation play out.

The Bank is caught between two forces pulling in opposite directions — an economy that desperately needs rate cuts, and an inflation risk that won't allow them.

The majority view from Canada's major financial institutions is a hold throughout 2026.

Their reasoning is straightforward: hiking rates into a weakening economy would make everything worse. Less consumer spending, less business investment, less growth — leading to further slowdowns and layoffs. The exact opposite of what's needed.

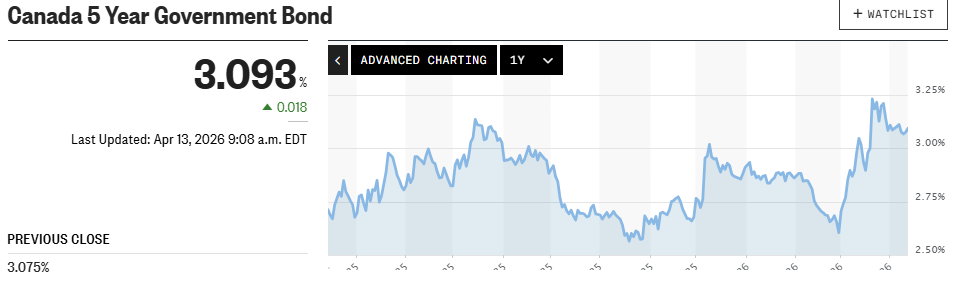

On the other hand, the bond market have priced in potential hikes — which matters directly for your mortgage.

There is a split in views.

The fixed vs. variable question right now.

Fixed rates have already priced in the possibility of those hikes. Variable is still materially lower. That gap exists because bond markets moved first — they anticipated the inflation risk and pushed fixed rates higher before any actual BoC decision.

It's also worth knowing that bond yields have been extremely volatile over the past two years.

If you look at a 2-year chart, yields have swung materially up and down with almost every major news event.

We've already seen multiple cycles this year where fixed rates crept higher on inflation fears, then slowly drifted back down as the situation evolved.

This is not a stable, predictable rate environment — every headline out, every jobs print, every inflation reading has the potential to move rates materially in either direction within days. I wouldn't take any rate prediction this year as a guarantee, including from Canada's largest banks — over the last few years forecasts have been revised, reversed and revised again within the same quarter.

But here's the other side.

If the Iran conflict resolves — peace deal, ceasefire, oil normalizes — rate hike expectations get priced out just as fast as they were priced in. A resolution could take it back to zero.

The key thing to watch is consumer inflation expectations — not actual inflation.

Here's something most people don't know. The Bank of Canada watches consumer inflation expectations as closely as actual inflation — sometimes more so.

When people expect inflation, they spend faster today, demand higher wages, and businesses raise prices preemptively — which can actually create the inflation they feared.

Nobody fully understands exactly how or when this translates into real inflation — it's one of those relationships that's messy in practice but universally accepted in economic theory — but what central banks do know is that once expectations become unanchored, they're extremely difficult to reverse. That's why the BoC treats them as a leading indicator rather than waiting to see actual inflation show up in the data first.

The Bank has been clear: they won't hike to fight an oil supply shock.

But they will hike if Canadians start expecting persistent inflation and change their behaviour because of it. We get the next quarterly reading on expectations shortly. If they've moved materially higher, the calculus shifts. If they haven't, the hold camp wins and variable looks increasingly attractive.

What this means if you have a decision to make.

Nobody — not the banks, not the markets, not the BoC itself — knows with confidence which way this resolves. That uncertainty is exactly the environment where getting your mortgage structure right matters more than trying to predict the outcome.

If you're renewing soon, the window to think this through carefully is narrowing.

Book a Call or respond to this email to discuss your situation further.