Self-Employed Mortgage in Toronto: How to Qualify When Your T4 Doesn't Tell the Full Story

Here is the problem most self-employed borrowers run into.

You earn $250,000 a year. Your accountant does their job well and reduces your taxable income to $90,000. You go to the bank for a mortgage and they qualify you on $90,000.

On paper, you look like someone who earns less than the junior employee across the desk from you. You get declined, or you get approved for far less than you can actually afford. And the frustrating part is that the write-offs causing the problem are the same write-offs that are building your actual financial position.

This is the core tension of self-employed mortgage lending in Canada. The tax system rewards you for writing off expenses. The mortgage qualification system penalizes you for it. Navigating that gap is what I specialize in.

Why Banks Struggle With Self-Employed Income

A bank looking at a T4 employee sees predictable, documented, guaranteed income. The number on line 15000 of the tax return is what goes into the qualification formula.

A bank looking at a self-employed borrower sees a notice of assessment with net income after deductions. The $180,000 in business expenses that reduced your income from $250,000 to $70,000 is legitimate under CRA rules. But from the bank's perspective, they can't easily verify whether that $70,000 net income reflects true cash flow or a structural write-off strategy.

The result: most big bank lenders apply their standard qualification formula to the net income figure, which often dramatically understates what the borrower actually earns and spends.

The solution is not to stop writing off expenses. The solution is to use lenders and products that are designed to handle self-employed income properly.

How I Approach Self-Employed Qualification

True cash flow analysis first. Before I look at lender options, I want to understand what you actually earn and spend. For most self-employed clients, the gap between gross revenue and net taxable income is significant, and some portion of those deductions (vehicle, home office, depreciation) can be added back to produce a more accurate income picture for qualification purposes.

Two-year average where it helps you. If your income has grown over the last two years, lenders who average the two years may understate your current position. I look for lenders who will use the most recent year, or weight the calculation toward the current year's trajectory.

Bank statement programs where they fit. Several lenders offer bank statement mortgage programs that qualify you based on 12 to 24 months of business deposits rather than tax return income. If your deposits reflect true cash flow significantly higher than your taxable income, this is often the clearest path to the mortgage you actually qualify for.

B-lender bridge where needed. If your income history is short (under two years self-employed) or your NOA income simply is not enough for A-lender approval, there are B-lenders who will approve based on stated income with a higher down payment. The rate is higher, but it is a two-to-three year bridge, not a permanent solution.

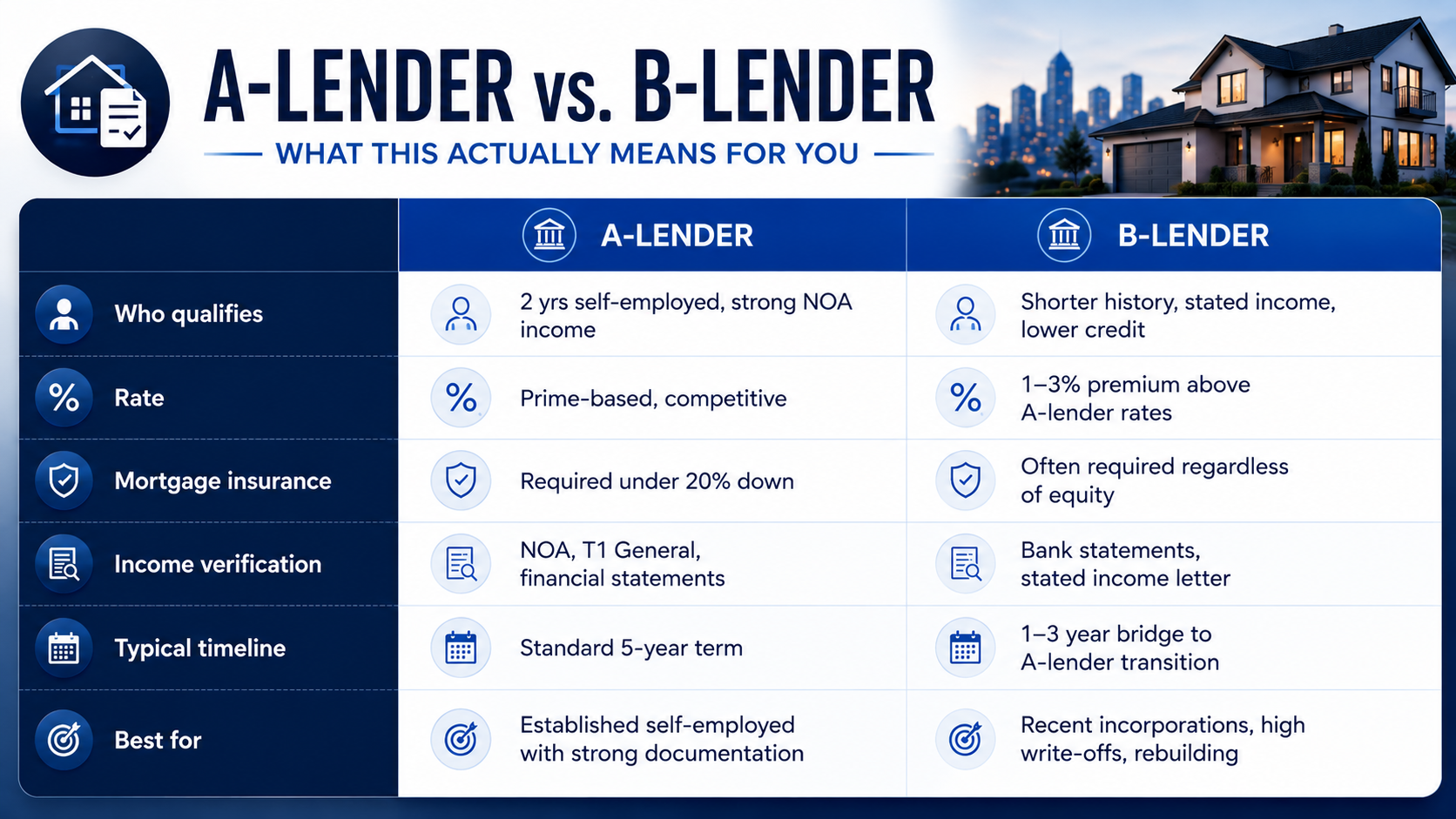

You Can Qualify as Self-Employed on the A-Side Too

A common assumption is that being self-employed automatically means B-lender rates. That is not the case.

A-lenders including major banks and credit unions do approve self-employed borrowers. The requirements are more demanding, but the path is available. Generally you need two full years of self-employment history, NOA income that clears the stress test at the purchase price you are targeting, clean credit, and documentation that tells a coherent income story.

The place where most self-employed borrowers get stuck at A-lenders is not their actual income. It is how their income appears on paper after deductions. This is where addbacks matter. If a lender will allow vehicle, home office, and CCA (depreciation) deductions to be added back to your declared income for qualification purposes, the number on your NOA becomes the floor, not the ceiling.

Not all A-lenders are equally flexible on addbacks. Part of what I do is match your specific income profile to the lender whose underwriting approach gives you the best qualification number. The same borrower can get very different results depending on which A-lender reviews the file.

The B-lender path is not a failure. It is a structured bridge. I have moved dozens of self-employed clients from B-lender approvals into A-lender products within 18 to 36 months by restructuring how income is documented and improving the overall financial picture.

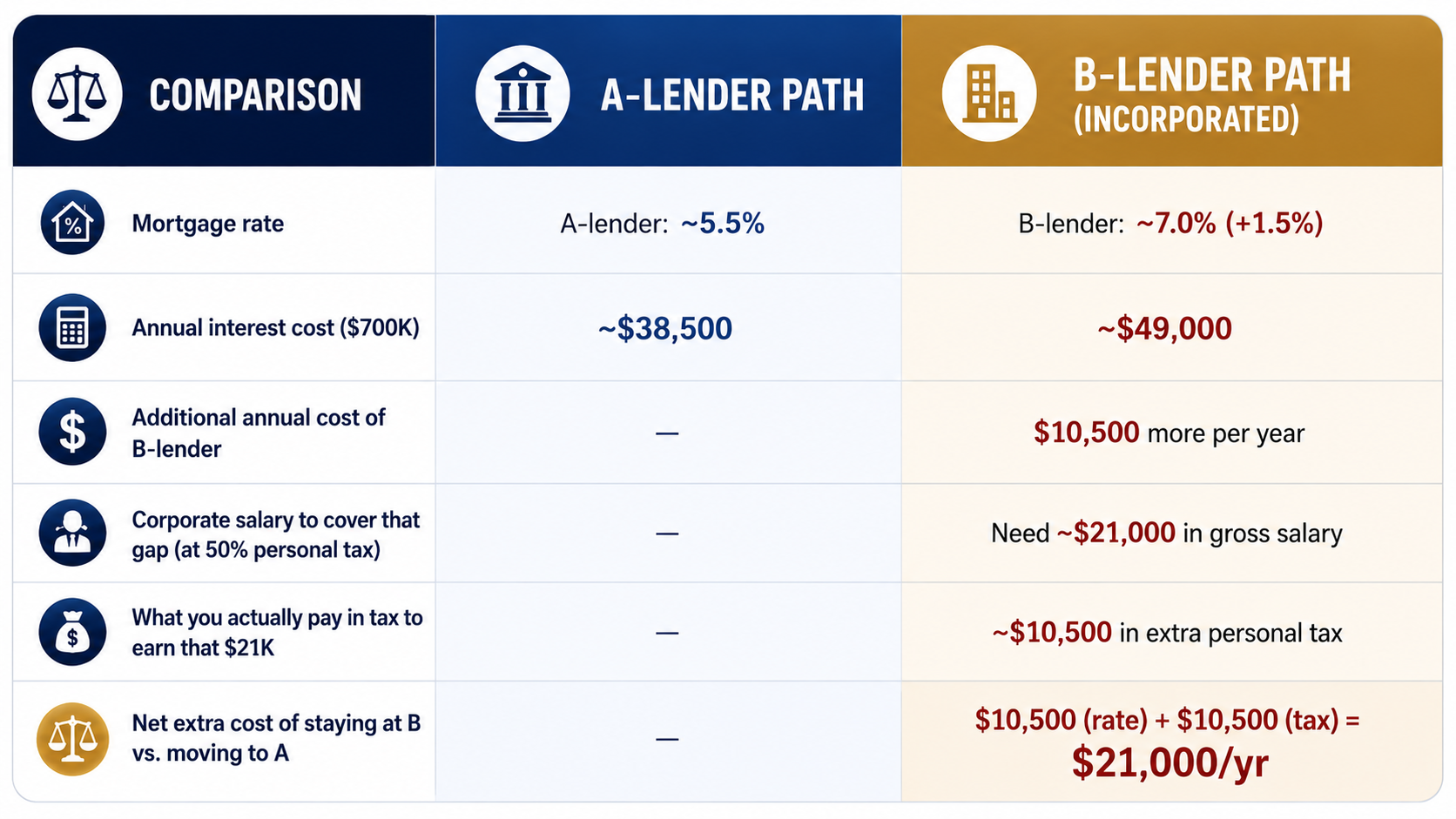

The Real Cost of Staying at a B-Lender: A Tax Analysis

This is a calculation most borrowers never see, and it changes how you should think about the A-versus-B decision.

The typical framing is simple: B-lenders charge 1 to 2% more. On a $700,000 mortgage that is $7,000 to $14,000 per year. Annoying, but manageable.

But for incorporated borrowers, there is a second cost that almost nobody mentions.

To cover that extra mortgage cost from your corporation, you need to pay yourself more salary or dividends. If you are in a 50% personal marginal tax rate, every dollar of extra mortgage cost requires roughly two dollars of gross corporate income to fund it. The tax on that corporate-to-personal transfer is not free.

The actual total cost of staying at a B-lender for an incorporated borrower in a high tax bracket is often close to double what the rate difference suggests on paper. The 1.5% rate premium feels manageable until you account for the tax you pay to generate the money to cover it.

This does not mean the B-lender path is wrong. Sometimes it is the only path available right now. But it means the cost-benefit analysis needs to include the tax layer, not just the rate difference. That calculation is something I do with every incorporated client before we decide which direction to go.

The Path From B-Lender Back to A-Lender

Year 1 to 2: Maintain the B-lender mortgage, make all payments on time, and build a clean credit history. Work with your accountant to structure income documentation more clearly for mortgage purposes. This does not mean reducing write-offs. It means ensuring income can be documented in a way A-lenders can work with.

Year 2 to 3: At renewal or when you hit a trigger point, approach A-lenders with two full years of clean self-employment history. With proper documentation and strong credit, many clients qualify for A-lender products at this stage.

The rate difference between B and A products is typically 1 to 2% annually. On a $700,000 mortgage, that is $7,000 to $14,000 per year. Add the tax layer described above and the number is often higher. The transition is worth planning for from day one.

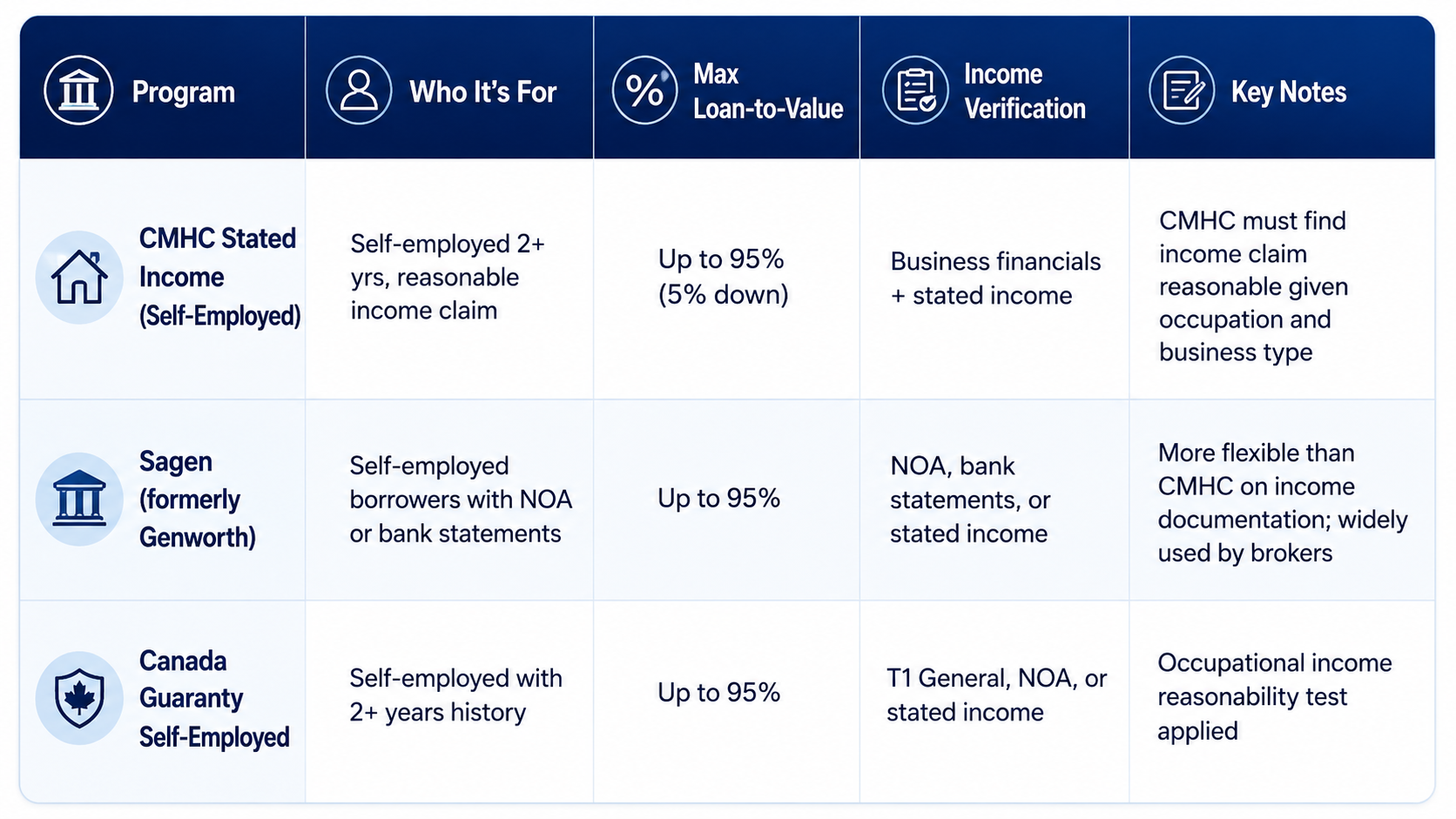

Self-Employed Insured Mortgages: Yes, They Exist

Most self-employed borrowers assume mortgage insurance (CMHC, Sagen, Canada Guaranty) is only available to T4 employees with a predictable paycheque. That is not accurate.

All three Canadian mortgage insurers offer programs specifically designed for self-employed borrowers. This means that if you have less than 20% for a down payment, you can still access insured mortgage financing as a self-employed individual, including stated income programs.

Here is how the insured self-employed programs work: instead of proving income through a standard T4 or NOA, you provide evidence of self-employment (two years of business history, GST/HST registration, business license or accountant letter) and state the income you are earning. The insurer then assesses whether that stated income is reasonable based on your occupation, business type, and years in operation.

The key phrase is "income reasonability." An accountant who has reduced your taxable income to $60,000 through write-offs does not mean you state $60,000 to the insurer. You state what you actually earn from the business, before write-offs. The insurer asks whether someone in your field, with your years of experience and business type, could plausibly earn that amount.

Important: insured mortgages require the property to be owner-occupied and the purchase price to be under $1.5 million. For higher-priced Toronto properties this may not apply, but for first-time buyers and those moving into starter homes in the $700K to $1.2M range, this is a significant option that often gets overlooked.

If you have been told you cannot get mortgage insurance as a self-employed borrower, that information may simply be incorrect, or it may be that whoever told you was not familiar with these programs. A broker who regularly works with self-employed clients will know how to structure the file for insurer approval.

Incorporation: What It Changes and What It Doesn't

A common misconception: if you incorporate your business, mortgage qualification becomes easier.

It doesn't. In fact, it often creates a new layer of complexity.

Most banks will not use corporate income for personal mortgage qualification unless you can document salary or dividends paid to yourself. If your corporation retains earnings, those earnings are not accessible for qualification purposes without a dividend declaration. And declaring dividends purely for mortgage qualification has tax implications.

Incorporated borrowers typically need two full years of T4 salary and/or T5 dividends to qualify on that income. If you are early in your incorporation or your corporation retains most earnings, the qualification picture is usually more limited than it was as a sole proprietor.

This is worth knowing before you incorporate, not after. If the mortgage is coming soon and you are considering incorporation, talk to both your accountant and your mortgage professional before making any structural changes.

What Toronto's Market Means for Self-Employed Borrowers

Toronto's average detached home price sits above $1.2 million. The stress test at current rates requires you to qualify at roughly 2% above your contract rate.

For a self-employed borrower targeting a $1.2 million property with 20% down, you need to show approximately $220,000 to $240,000 in qualifying income to clear the stress test at today's rates. If your NOA shows $90,000 after write-offs, that gap is significant.

This is exactly the situation where lender selection and income structuring matter most. I regularly work with clients who have been turned down by their primary bank and end up qualifying through a bank statement program or a lender with a more sophisticated approach to self-employed income assessment.

The approval exists. It just requires knowing where to look and how to present the file.

What I Need From You to Get Started

To assess your qualification options, I typically review the following:

Two years of notices of assessment and T1 General returns. This tells me what the standard qualification picture looks like and where addbacks might be available.

12 to 24 months of business bank statements. Even if you plan to go the A-lender route, having these ready gives us flexibility.

A summary of your business structure (sole proprietor, incorporated, partnership) and how long you have been operating in the current structure.

Your credit report. For most clients I work with, this is not the issue. But it is part of the full picture.

From there, I can map out which lenders are realistic, what income needs to look like to hit a specific purchase price, whether insured financing is available to you, and whether any income restructuring before application is worth pursuing.

⚠️ Do Not Attempt Cash Damming Without Professional Guidance

Cash damming involves mortgage structuring, tax deductibility, leverage risk, CRA tracing requirements, and ongoing bookkeeping discipline. Mistakes in execution can invalidate deductions, create CRA reassessment exposure, increase financial stress, and compromise long-term strategy performance. Before implementing cash damming, speak with a qualified mortgage professional, an accountant experienced with CRA tracing requirements, and a tax advisor familiar with leveraged deductibility strategies.

Austin Yeh is a Smith Manoeuvre Certified Professional and independent mortgage agent based in Toronto, funding mortgages across Canada. He specializes in advanced mortgage strategies for high-income earners, real estate investors, and self-employed borrowers.

Lender features and policies are subject to change. Always verify current product details directly with the lender or through an SMCP-certified mortgage broker. This article is for educational purposes and does not constitute financial or mortgage advice.